Reshaping Agrochemical Portfolios: Creating Value Through Innovation, Specialization, Sustainability, and Integration

Executive Summary:

The global agrochemical market is estimated to cross $420 billion by 2032. At present, it is being reshaped by sustainability imperatives, tightening regulations, and precision agriculture. Agrochemical producers are moving towards biological and hybrid solutions while rationalizing their businesses to focus on differentiated, high-growth, and integrated offerings. End-to-end value chain integration, bio-based innovation, operational separation, and strategic specialization are surfacing as the decisive layers for securing long-term competitive advantage and value creation. To gain an upper hand, companies must actively prune their low-value SKUs and reallocate R&D and capital towards regulatory-resilient, sustainability-aligned, differentiated portfolios.

Why Portfolio Management

Agriculture is facing a major transformation as it seeks to produce more to feed the growing population and at the same time minimize the impact of farming on the environment. Governments are limiting or banning the use of the most hazardous synthetic chemicals. For instance, the US banned Dimethyl Tetrachloroterephthalate (DCPA or Dacthal), India banned Carbofuron 50% SP, and the United Kingdom banned the neonicotinoid pesticide Cruiser SB. To remain profitable in a landscape of fluctuating raw material costs and geopolitical conflicts, and at the same time competitive, complying with laws to avoid the cost of legal action or product recalls, all while maintaining capital discipline, agrochemical producers must optimize the footprint of their assets.

Agrochemicals Market: Accelerating Growth through Innovation and Sustainability

The agrochemicals market is estimated at around USD 300 billion by 2026 and forecasted to reach more than USD 420 billion by 2032, growing with a CAGR of 4.5-5.5% during the forecast period. The agrochemical market continues to grow due to higher dependence of major global crop systems on consistent nutrient supply, weed control, disease management, and yield protection across vast acreages of cereal, oilseed, and horticultural crops. The agrochemical resistance pressure, regulatory screening, and precision application tools push buyers toward differentiated chemistry, specialty fertilizers, and service-linked offerings, driving the growth of high-value agrochemicals. Demand for agrochemicals in the Asia-Pacific region is expected to be the highest due to the need to produce higher crop yields to feed the growing population in the region, while North America and Europe are seeing the development of premium agrochemicals. The key players in the market, including BASF, Bayer, and Syngenta, are strategically enhancing their geographical reach in the emerging markets of Asia-Pacific and Latin America. The industry giants are actively engaged in the research and development of sustainable solutions to comply with environmental and food safety regulations.

Changing Agrochemicals Landscape

Dynamics of Changing Agrochemicals Landscape

The agrochemical landscape is moving faster from broad-spectrum synthetic formulations towards precision-applied hybrid (semisynthetic) and biological solutions. Driven by climate change, resource scarcity, and evolving environmental and food safety regulations, the industry is focusing on maximizing yield and minimizing chemical residues and environmental impact.

Evolving Regulatory Trends Shaping the Agrochemicals Market

Strict environmental regulations such as the Farm to Fork framework of the European Union and global chemical management rules ban or limit the historically common active ingredients such as neonicotinoids and glyphosate. Neonicotinoids, a widely used group of insecticides used in the US, are facing higher regulatory restrictions due to risk to pollinators. Following the recent ban of all emergency authorizations of neonicotinoid pesticides by the EU, in 2025 the UK also banned emergency use of Cruiser SB, a highly toxic neonicotinoid to bees. The evolving regulations are significantly affecting pesticide consumption. For instance, the EU’s ambitious plan called the Framework for Sustainable Food Systems (FSFS) regulates pesticide use along with aspects like biodiversity, healthier diets, and sustainable food sources and logistics. The EU aims to reduce the use of chemical pesticides by 50% by 2030 and fertilizer use by 20%. Such regulations are promoting the development of traceable, bio-based, and sustainable agrochemical solutions.

Development of Bio-based and Hybrid Agrochemicals as a Game Changer

The industry is moving towards agricultural biologicals, which include biopesticides, biostimulants, and biofertilizers. Unlike traditional large-scale use of broad-spectrum insecticides, growers are using species-specific agricultural pheromones for mating disruption and precision pest management. These solutions are leaving virtually zero residue. Agrochemical manufacturers are utilizing genetically engineered nitrogen-fixing bacteria and seaweed extracts such as those being tested in EU-funded initiatives like BioCorp to improve crop nutrient uptake and stress tolerance. The development of biological formulations and their increasing demand is witnessing higher growth driven by strict environmental and food safety regulations, especially in European and North American countries.

Major agrochemical manufacturers and innovators are balancing conventional chemistry with sustainable biologicals by shifting towards ‘hybrid pest control’. The hybrid or semi-synthetic agrochemicals are being manufactured by blending synthetic chemicals with naturally derived agents like microbes, alongside digital agronomy, to reduce chemical usage while maintaining higher crop yields. For instance, STK bio-ag technologies developed Regev, a hybrid pesticide, a premix of a synthetic pesticide with a botanical-based biopesticide. The hybrid pesticide helps to tackle regulatory liabilities by reducing synthetic chemical load on the environment. The use of biopesticides is forecast to grow at a significant annual rate of 15% to 20% in the near future, while consumption of synthetic chemicals is forecasted to grow by 3% per annum in the foreseeable future. These growth rates indicate the transition towards higher consumption of biopesticides or semisynthetic pesticides than synthetic pesticides.

| Company | Bio-Based/Hybrid Product | Year | Features |

| BASF | Poncho Votivo Precise Seed Treatment | 2023 | It contains the Bacillus firmus I-1582 bacteria, which creates a living protection barrier against two generations of nematodes. |

| Novozymes A/S | Taegro | 2020 | Novozymes A/S partnered with Syngenta and officially launched Taegro, a broad-spectrum, microorganism-based biofungicide and bactericide. |

| STK bio-ag technologies | Regev | 2018 | A hybrid pesticide, a premix of a synthetic pesticide with a botanical-based biopesticide. |

| Bayer | Sonata | 2020 | Biofungicide developed from a naturally occurring, patented strain of the soil bacterium Bacillus pumilus (strain QST 2808). |

Precision Agriculture Affecting the Consumption of Agrochemicals

Application of agrochemicals is witnessing a faster revolution with rapidly growing digitalization and the emergence of Artificial Intelligence (AI) assisted tools and equipment. AI-enabled tractors and drones are enabling the identification of weeds and diseases in real time. This enables farmers to spray only the affected area, significantly lowering the volume of herbicides and pesticides that were traditionally used to spray the entire field. The rise of “Outcome-Based Pricing” is the result of this shift, which separates a chemical company’s revenue from the actual volume of product sold. Instead of paying the provider for the volume delivered, this model links payment with the cleanliness of the field or the final yield. Additionally, this change makes it possible to employ “hyper-potent” molecules that were previously too costly or hazardous for the field as a whole.

Formulation technologies such as the development of nano-agrochemicals are rapidly advancing, supported by public funding to avoid unnecessary soil pollution and degradation. For instance, Indian Farmers Fertilizer Cooperative Limited developed Nano Urea in 2021 and began its commercial production in June 2021. The coated agrochemical formulations release their ingredient slowly, aligned with the growth stages of the plants and reducing chemical runoff into water systems.

Supply Chain Constraints Shaping the Regional Production

Geopolitical shifts and post-pandemic protectionism for inventory corrections are drastically altering the global supply chain. For instance, war between Iran and the US significantly impacted the crude oil supply chains; Asian countries dependent on Middle Eastern imports were severely impacted. This has resulted in a rise in prices of fertilizers, which are mainly produced from petrochemicals and petroleum gases. The US-China trade war has significantly affected the agrochemicals supply chains since China historically dominates the manufacturing of active ingredients. However, countries like India are evolving faster as alternative exporters for the agrochemical industry. For instance, according to India Brand Equity Foundation, India emerged as the third largest agrochemical exporter in FY 2025 by witnessing agrochemical exports of USD 3.3 billion from agrochemical exports of 1.5 billion in FY 2015. Distributors and farmers are focusing on strategic fulfillment and risk management rather than relying on massive and consolidated stockpiles of traditional inputs.

Portfolio Rationalization

The agrochemical producers are diverting their focus and resources from low-margin and off-patent commodities towards differentiated, high-growth and sustainable solutions, integrated crop protection solutions, biosolutions, and patented formulations. Players are optimizing their portfolios in multiple ways:

1. Unlocking Value through Business Specialization

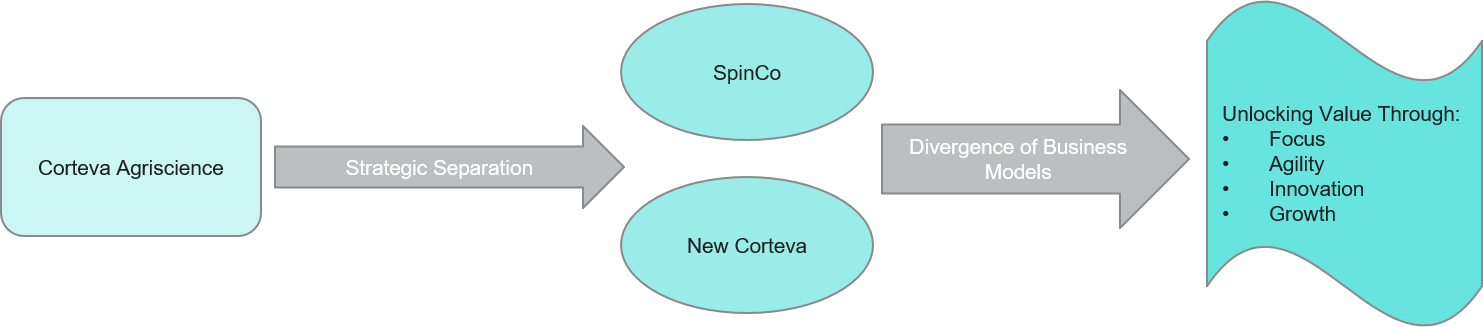

The agrochemical companies are taking deliberate steps and investing in high-return endeavors to reduce costs and ensure higher impact to farmers and maximum returns to the company. The companies operating in broader verticals of the agriculture industry are specializing in their individual business portfolios through strong strategic and operational focus, tailored capital allocation strategy, greater ability to leverage evolving market dynamics to deliver consistent returns, and separate investment profiles unlocking greater value for shareholders. For example, Corteva Agriscience, a leading global agriculture technology company, has planned to separate the company into two independent publicly traded companies, one comprising its seed business (SpinCo) and the other comprising its crop protection business (New Corteva). The separation is scheduled to be completed in the second half of 2026. Looking to the future, with the separation of these two businesses, Corteva aims to maximize long-term value creation by focusing on their own priorities.

The separation of Corteva Agriscience into two distinct companies reflects a divergence in the business models of seeds and crop protection. While seeds are essentially high-margin biotech platforms that require longer regulatory and breeding cycles, crop protection relies on faster-moving chemistry and biologicals. The split will allow companies to evaluate them as focused technology companies rather than generalized agricultural conglomerates.

2. Operational Separation

The prominent industry leaders operating across the world with agrochemicals as a leading business segment use structured steering to differentiate between core chemical operations and specialized agricultural units to maximize capital allocation. The chemical companies that find a place as a leading agrochemical company are actively focusing on their agriculture business to gain a competitive edge in the market. The companies are putting a higher focus on cash and strengthening capital discipline by lowering capital expenditure and continuing their cost-saving programs. For instance, BASF is setting a new direction through effective portfolio management, capital expenditure, and performance enhancement.

3. Repositioning the Portfolio around Sustainable Agriculture Solutions

Taking into consideration the tightening environmental and food safety regulations, agrochemical producers are reshaping their portfolio towards relatively sustainable and low-environmental impact formulations. The companies are systematically reducing their dependence on synthetic chemicals while increasing investment in hybrid and completely biological solutions. The companies are evaluating their portfolios based on regulatory risks, long-term market attractiveness, and sustainability metrics. The hybrid formulations combine natural products with site-specific synthetic chemicals, enabling the production of effective pesticides with different modes of action. The hybrid combination has lower environmental impact, enables resistance management, and is highly suitable for integrated pest management programs. For example, STK Bio-Ag Technologies has undertaken the development of several hybrid and biological formulations. With this innovative and strategic transition, the company is building a sustainable agrochemical platform delivering productivity and sustainability benefits.

4. Building End-to-End Agricultural Value Chain by Portfolio Integration

The recent geopolitical conflicts and trade wars significantly impacted the agrochemical value chain, underlining the need for integrated value chains. This has resulted in agrochemical companies developing a holistic agrochemical ecosystem that encompasses seeds, biologicals, crop protection, and digital farming tools to move beyond product sales and become a strategic partner across the entire farming cycle, capturing more value along the agriculture value chain and enhancing customer retention and differentiation. This integrated ecosystem approach is enabling companies to enhance recurring revenue streams, improve product adoption rates, and strengthen competitive position in the market.

Conclusion

The evolution of stringent environmental regulations, development of precision agriculture techniques, rising focus on innovative and bio-based solutions, and the geopolitical factors shaping agrochemical production necessitate effective agrochemicals portfolio management to remain competitive in the highly competitive agrochemicals industry. Elimination of low-value SKUs helps in increasing manufacturing capacity, R&D budgets, and working capital by reallocation of these budgets to high-value formulations. The integration of the value chains enhances supply chain efficiency. Innovative efforts to comply with evolving regulatory trends ensure compliance with developing global safety standards, providing a competitive edge and reducing vulnerability to legal liabilities. Regulatory restrictions are now catalyzing revolutionary change in the agrochemicals industry rather than obstacles to advancement. The stories of Corteva Agriscience, BASF, Bayer, and Syngenta highlight the crucial role that cooperation, innovations, standardized laws, and consistent investment play in shaping the global agrochemicals industry toward a resilient and sustainable future.

As a strategic intelligence partner, Stellarix is working with chemical suppliers, agrochemical manufacturers, regulatory agencies, and end users to ensure sustainable growth of the agrochemicals industry. We bring with us technology intelligence, intellectual property insights, regulatory knowledge, and competitive market understanding that links science and business objectives.

Let's Take the Conversation Forward

Reach out to Stellarix experts for tailored solutions to streamline your operations and achieve

measurable business excellence.