How Startup Disruption is Reshaping the Agrochemicals Industry from Compliance to Crossroads?

Key Takeaways:

- The constantly rising renewal cost per molecule is creating additional pressure on mid-level manufacturers

- The development timelines are no longer compatible with the market’s disruption cycle

- By building around failure points, startups are carving a new silver lining for agrochemical market players

The agrochemical industry is no longer debating the pace of transition from synthetic pesticides; it has embraced the change. The focus is now on realigning operations with emerging parameters and expectations of various stakeholders of this value chain.

As per Stellarix’s observation, the global crop protection market is valued at approximately $85.6 billion. While the numbers look exceptionally good on the surface, they tell a tale of contradiction within. On one hand, biosolutions are gaining traction at a CAGR of 13-17%; synthetic fungicides and insecticides are being squeezed under regulatory and consumer pressures. On the other hand, mid-level agricultural chemical companies aren’t able to afford the development of new active ingredients, and are also failing to compete with generics on prices outside China and India.

This segmentation is widening further, paving the way to a new class of startups that are navigating the forces driving this fracture. This article assesses the forces fragmenting this segment and classes of startups that are emerging as a result of that gap.

Understanding the Forces Fragmenting the Agrochemicals Sector

The Strengthening Regulatory Wall

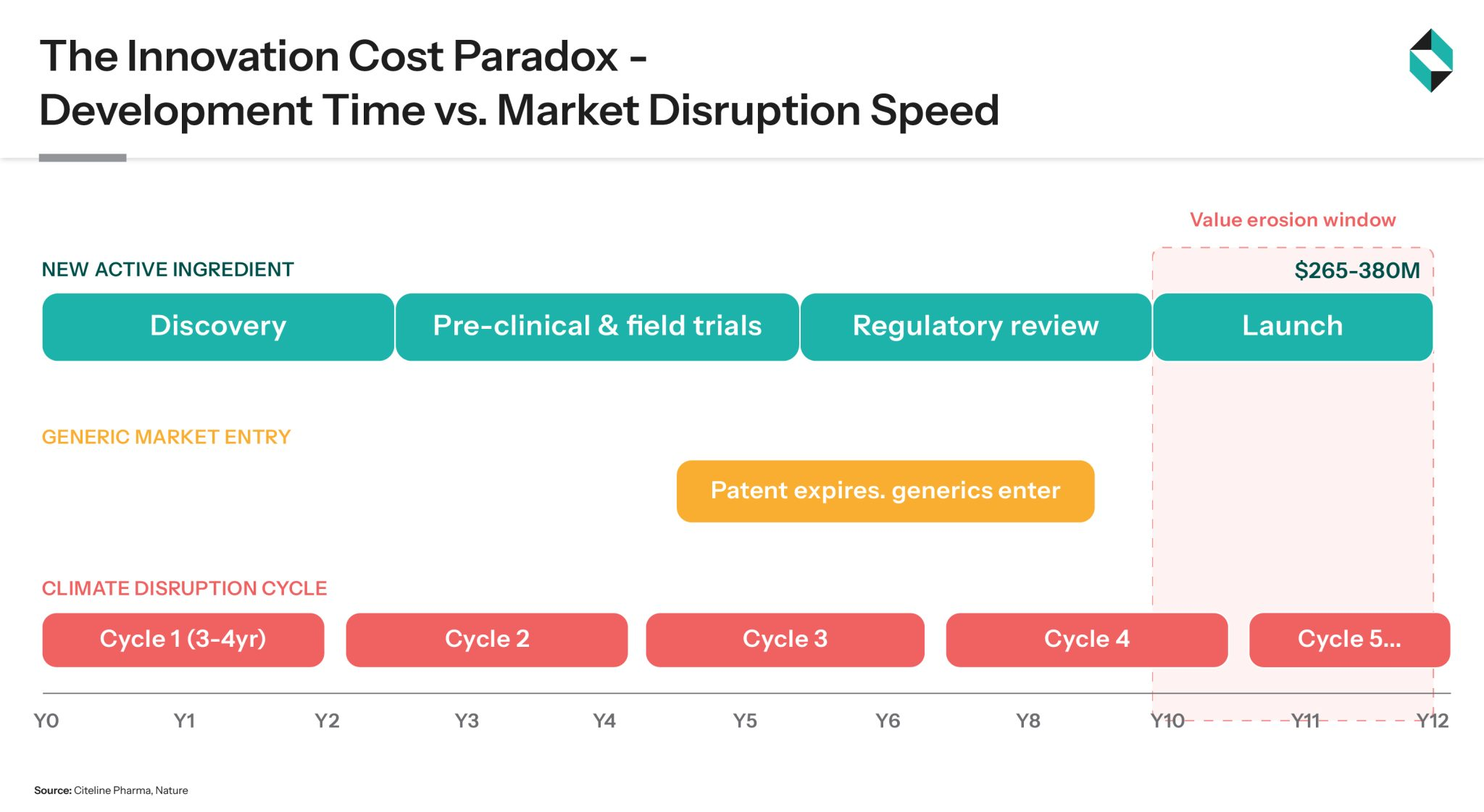

When the European Union authorized glyphosate in 2023, it was a reprieve. However, the active ingredient pipeline is a completely different story. During the 1107/2009 review, the EU reviewed over 50 substances, and none of them received renewal since 2018. The regulatory risk premium implied on them made it economically irrational to defend them.

At present, the cost of keeping a synthetic active ingredient in the EU market is between € 500,000 and € 965,000. Companies that earlier earned revenue from mancozeb and chloropyrifos are now rebuilding their complete portfolios without any guarantee that the next molecule will pass the present hazard-based criteria.

The Generic Pressure of Patent Cliffs

Patent cliffs were always assumed on product and growth roadmaps. What wasn’t assumed was the speed at which Indian and Chinese companies would compete on formulation innovation, along with active ingredient synthesis. Consequently, molecules expected to generate stale margins in the next few years are being traded at 15-25% in emerging markets.

India, Southeast Asia, and Brazil are currently the most aggressive generic battlegrounds. Companies like Syngenta and Bayer-acquired Monsanto that earned premiums during the 2018-2022 consolidation period are now running thin on margins and profits.

The companies with aggressive growth charts aren’t necessarily with big R&D budgets. However, most of them are successfully building data proximity to farmers and turning channel disruption into a first-mover advantage rather than a challenge. – Stellarix Observation

The Demand-Supply Imbalance due to Climate Impact

The diseases and pest patterns are emerging faster than product portfolios. For instance, the fall armyworm (Spodoptera frugiperda) has raised demand for a new class of fungicides and insecticides in the last five years across South Asia and Africa. Similarly, several drought-resistant weed species are outpacing the existing efficacy profiles of herbicides. Most geographies are now being colonized by advanced fungal strains that needed no treatment earlier.

Developing a new strategy usually takes around 10-12 years while costing over $300 million. Here is where the math gets uncomfortable, as companies cannot make long-term bets on pest geographies that are evolving at an unpredictable pace.

The Fragmented Distribution Channels

Precision application technology is helping manufacturers reduce total consumption without sacrificing output quality. Various advanced approaches, including drone-based targeted delivery, AI-powered crop scouting, and variable-rate application systems, are narrowing total chemical use per hectare.

In North America, according to FBN, farmers plan to abandon the conventional distributors as soon as competitive pricing and formulation transparency are made public online. However, against normal assumptions, it wouldn’t take away revenues, but would bridge the gap between field-level data and agrochemical companies. Therefore, companies that control precision agriculture platforms will hold the key to ground-level intelligence.

The ESG Transition is Both Margin Dilutive and Capital Intensive

Institutional investors are swiftly moving beyond sustainability strategies as they are executing them with capital allocation. However, biosolutions and biological transitions are way more expensive than is being conveyed. For instance, just biopesticide registrations take 3-5 years minimum. Synthetic product registrations take somewhat the same time but have a longer market life. Any company aiming to transition its R&D efforts towards biologicals will need to accept a J-curve on profitability, something that wouldn’t be accommodated by quarterly earnings without intense investor pressures.

Pressures mapped. But where does this momentum lead? Our exclusive Agrochemicals Industry Outlook delves into market trajectory, portfolio realignment signals, and demand shifts reflecting how industry players are navigating the change in real time.

Which Startup Categories are Shaping Up Under these Pressures?

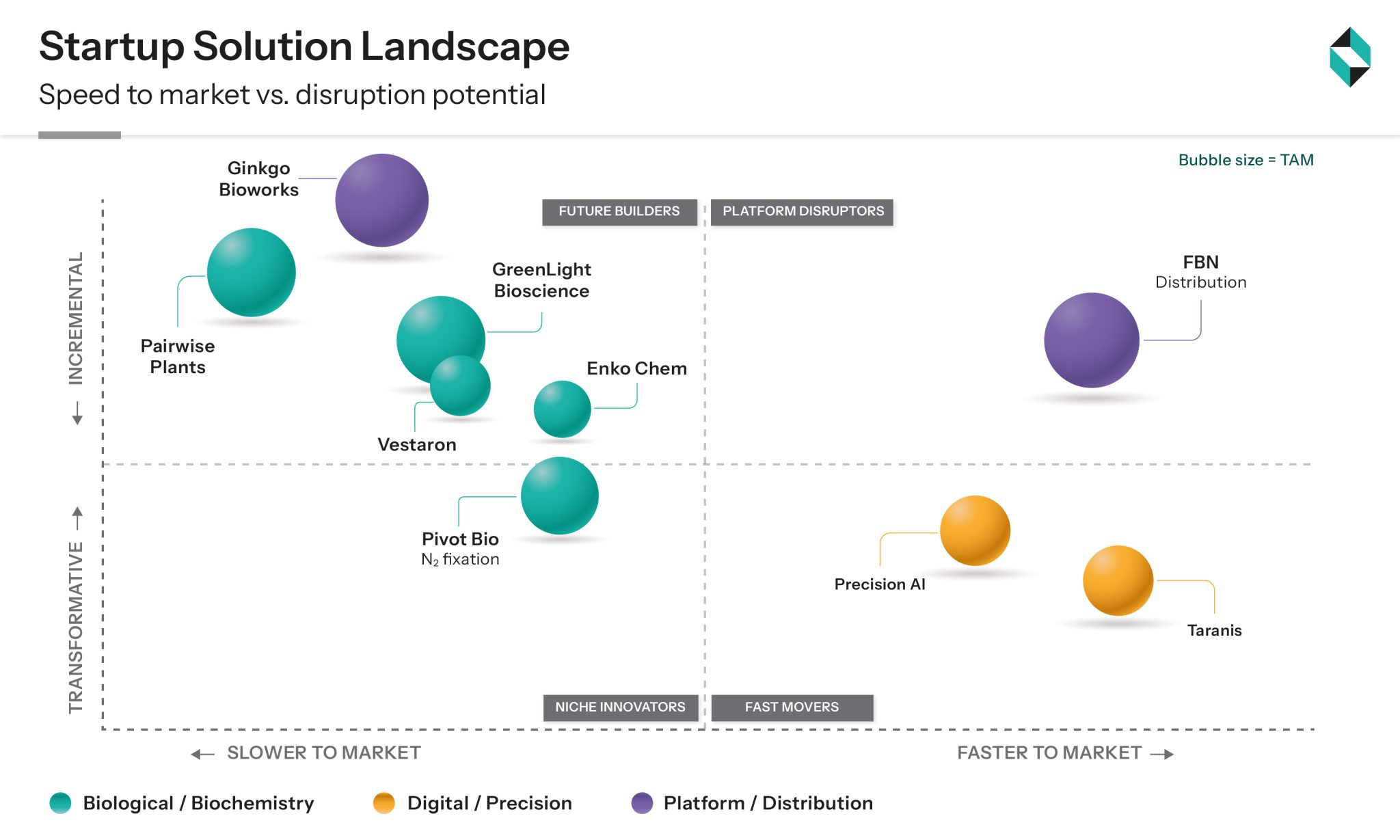

Basically, there are four startup categories that are emerging at the intersection of these pressures, solving not one but multiple challenges as they attract capital and strategic partnerships.

Biological Modes of Action

- Pivot Bio: A leading agricultural company that is engineering microbes to provide eco-friendly, microbial-based nitrogen to crops. By offering a strong alternative to synthetic fertilizers, it is reducing environmental runoff and emissions.

- Vestaron: The breakdown profiles offered by their spider-venom peptides are far superior to organophosphates.

- Enko Chem: The company is employing computational chemistry to design bioinsecticide candidates, costing a fraction of traditional screening methods.

Precision Application

- Precision AI: Their spot-spray tech is reducing herbicide requirements in canola and wheat by 70-90%.

- Taranis: The AI-powered field intelligence offered by them connects pest detection directly with application decisions. It is playing a key role in squeezing the agronomist-to-decision loop from days to hours.

RNAi and Next-Gen Biochemistry

- Green Light Biosciences: A pioneer of RNA-based modes of action in biopesticides, their non-GMP solutions specifically target diseases and pests without leaving any toxic residues or harming beneficial insects.

- Pairwise Plants: The company is employing CRISPR to develop disease-resistant crop traits. Such plants will have less dependency on fungicides and will thus need less protection.

Synthetic Biology Platforms

- Ginkgo Bioworks: They are engineering the platform infrastructure to enable the next-gen bioactive molecules discovery at a production scale. The intention is to collapse the development cost curve that presently favors only large-scale manufacturers.

Bottomline

None of the forces mentioned above poses a direct threat individually. However, their convergence makes the present conditions more complicated than cynical. It is daunting for any organization to handle generic competition, regulatory attrition, resistance evolution, and regulatory compliance without a structured portfolio transition strategy. If the balance sheets aren’t showing the signs now, they will in the near future.

What needs to be noted here is that these billion-dollar opportunities are not shrinking but bifurcating. Companies successful in balancing commodity chemistry with precision-enabled, sustainable, biologically enabled solutions will win this game.

How do you separate transition planning from transition theater? Stellarix works with agrochemical leadership teams to:

- Stress-test portfolio strategies against regulatory, competitive, and transition risk

- Identify emerging biosolution and precision agrochemical players representing partnership, acquisition, and disruption potential

- Navigate the inflection points in this segment

Let's Take the Conversation Forward

Reach out to Stellarix experts for tailored solutions to streamline your operations and achieve

measurable business excellence.