India’s Data Center Boom: Can Renewable Energy Keep up with Digital Growth

Executive Summary:

India is undergoing a data center boom that would not just empower its digital economy but also strain its energy infrastructure. The total capacity is estimated to triple up to 2, 500 MW by 2030. This growth is expected to attract investments worth $10 billion from domestic players as well as global hyperscalers. The energy demand accompanying this enormous growth will amount to 5-6 gigawatts by the end of this decade, which will be approx. 70% of the total electricity comes from coal. The core dilemma is whether the accelerating renewable energy push can align with the unprecedented 24.7 power needs of the data centers, and if this nation could turn this challenge into a model of sustainable digital growth.

India is undergoing one of the most transformative decades in its history. Digital infrastructure, AI, and clean energy are coming together to change India’s economy in a big way. But this change brings up an important question:

Can India’s renewable energy industry grow fast enough to keep up with the country’s rapidly growing data center industry?

This isn’t just a policy issue; it’s crucial to India’s digital future. Finding a balance between India’s goals of becoming a global data hub and a leader in clean energy is one of the decade’s biggest challenges.

The Rise of India’s Data Economy

India’s digital landscape has changed a lot in the past five years. With over 900 million internet users, expanding 5G coverage, and an ecosystem of digital-first enterprises, the country has become one of the world’s fastest-growing data economies.

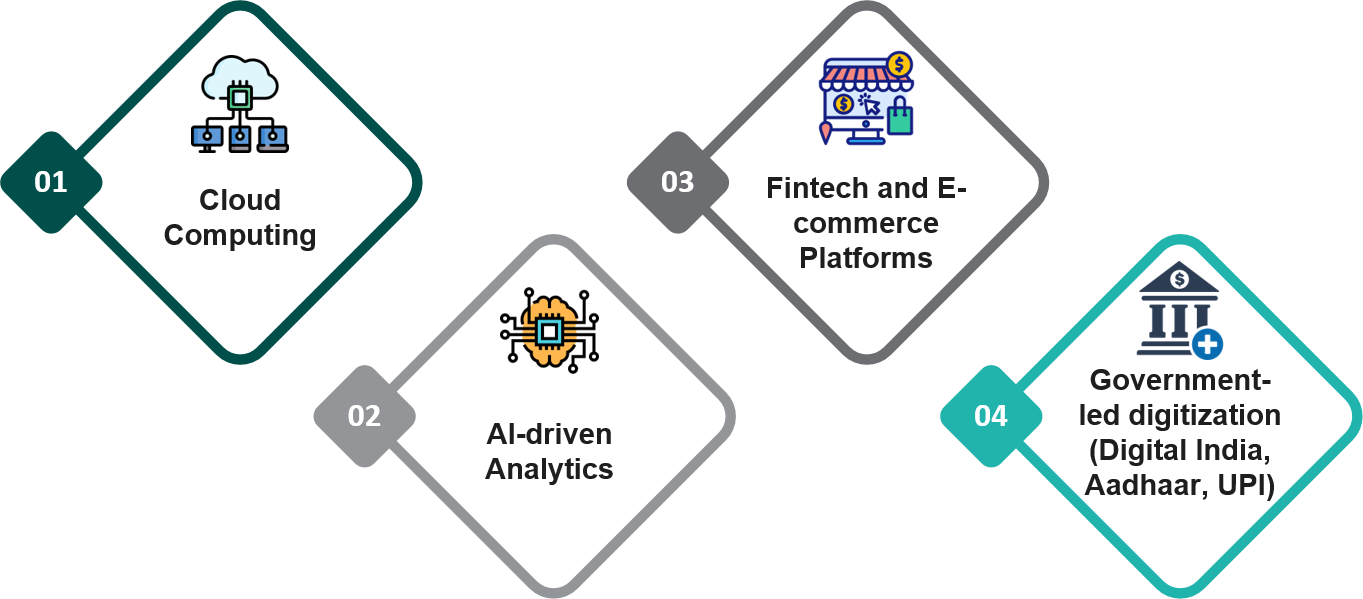

Cloud computing, AI analytics, Fintech, and e-commerce platforms, along with government-led digitization efforts like Digital India, Aadhaar, and UPI, have driven a huge demand for data generation and storage. A data center is a facility where thousands of servers run 24 hours a day, seven days a week. It handles every online transaction, streamed video, AI computation, and cloud service.

According to industry estimates, India’s data center capacity will grow from 870 MW in 2023 to more than 2,500 MW by 2030. This is almost three times as much. This growth is drawing over $10 billion in planned investments from big companies like:

- AdaniConneX, Yotta Infrastructure, and CtrlS are all working to help businesses grow in their areas.

- Global hyperscalers like AWS, Google, Microsoft, and Equinix are backing India’s role in the global cloud infrastructure.

But this kind of growth has an invisible but big cost: it uses a lot of energy.

The Energy Demand Challenge

Around the world, data centers use about 2-3% of all electricity and account for nearly 1% of carbon emissions. As AI training, edge computing, and real-time data analysis grow, this number is expected to increase significantly.

By 2030, India’s data centers will need 5 to 6 gigawatts of power. This is about the same amount of electricity as a city like Pune uses. Data centers need power continuously, unlike most industries. They run 24 hours a day and must stay online almost continuously, often requiring 99.999% uptime.

To meet this need, operators use more grid connections, diesel backup generators, and high-energy-consuming cooling systems. When these use power from fossil fuels, it makes it harder for India to move to clean energy. Right now, about 70% of the country’s electricity comes from coal. This strong dependence makes it harder to balance digital growth with environmental goals.

India’s Renewable Ambition: A Race against Time

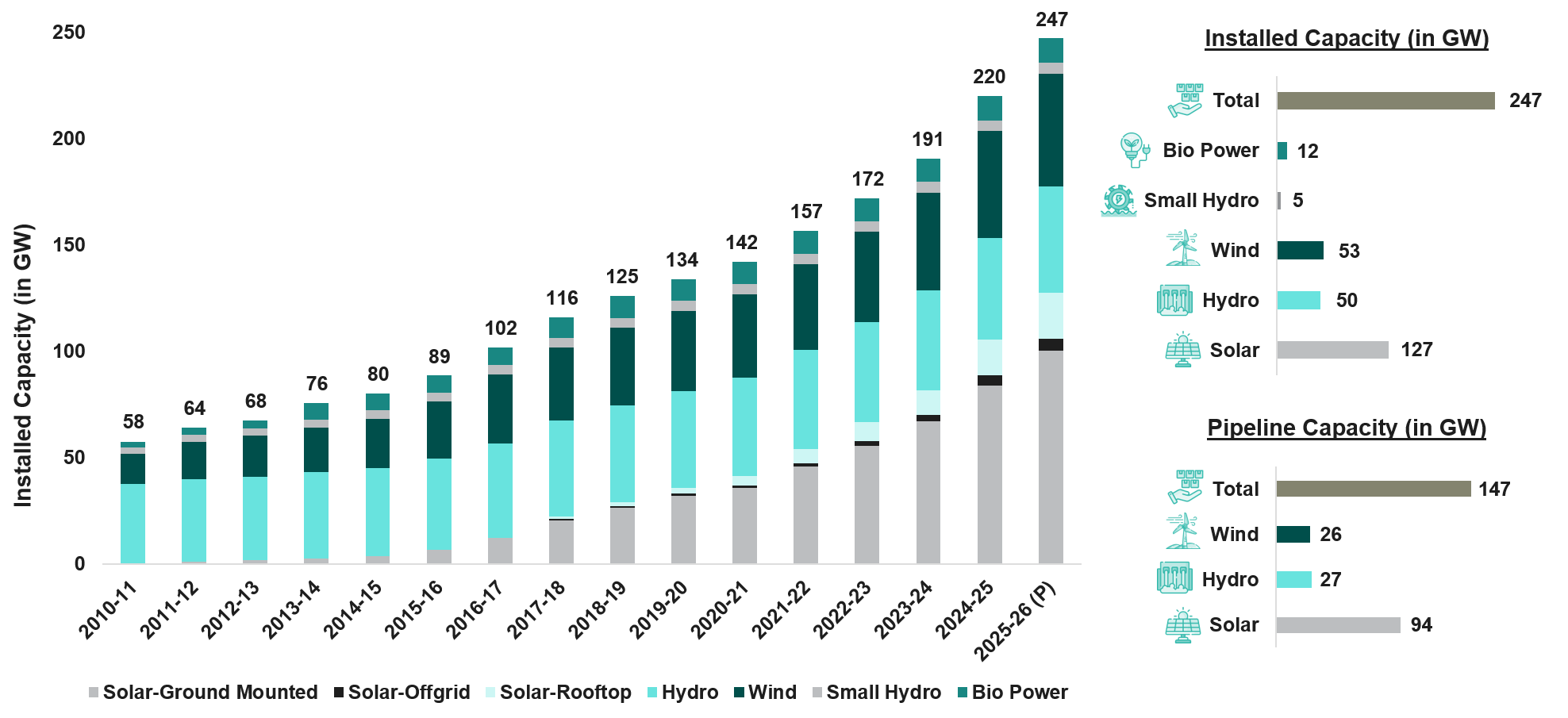

India is now seen as a leader in clean energy because of its work with groups like the International Solar Alliance (ISA) and its strong promises at COP28. By 2025, the country’s renewable energy capacity, including solar, wind, hydro, and biomass, will exceed 200 GW. India plans to reach 500 GW of renewable capacity by 2030, which would make up almost half of its total power generation.

As the graph shows, the rise from about 60 GW in 2010 to more than 200 GW now reflects ten years of steady policy support, investor trust, and initiatives focused on innovation. Key programs, like the National Solar Mission, Green Energy Corridors, and open-access reforms, have sped up the growth of renewable capacity. They have also improved grid connectivity and encouraged decentralized power generation.

However, the main challenge is keeping up growth at the right scale.

Data centers need a steady power supply, but renewable sources like solar and wind are not always available. Solar energy is strongest during the day, and wind energy changes with the seasons. To meet steady energy needs, the system requires:

- Battery Energy Storage Systems (BESS)

- Hybrid generation portfolios that include solar, wind, and hydro

- Flexible, smart grids

As the need for storage deployment increases, India’s large-scale energy storage capacity is still not enough. Right now, less than 2 GW is installed, but over 100 GW will be needed to reliably use renewable energy by 2030.

Stellarix assists enterprises in managing this shift by identifying and assessing new energy solutions, technological advancements, and strategic alliances that promote greener digital systems. To assist in connecting the expansion of renewable energy with the demands of the changing data economy, we map out solution providers, storage choices, hybrid energy models, and regulatory prospects. Stellarix facilitates well-informed decisions that connect digital progress to sustainable energy readiness by combining technological competence and commercial understanding.

Policy Landscape: Enabling a Green Digital Future

India’s policymakers are beginning to recognize this dual growth opportunity. They view data centers not just as digital infrastructure but also as big energy users that can support renewable energy needs. Key initiatives shaping this area include:

- Green Open Access Rules (2022): These rules let data centers and other big energy users buy renewable energy straight from suppliers without needing government permission.

- Data Center Policy (Draft 2020): This policy promotes the development of Green Data Parks powered by renewable resources and considers data centers part of the infrastructure sector.

- PLI Scheme for Advanced Batteries and Green Hydrogen (2021-2023): This program helps local production of energy storage, which is important for a steady supply of renewable energy.

- State-Level Incentives: States such as Maharashtra, Tamil Nadu, Telangana, and Uttar Pradesh provide financial benefits and quicker permits for environmentally friendly data centers.

These policies are helping India become a possible green digital center. They are bringing in big investments and more sustainable funding, especially as ESG rules become more important for businesses.

Industry Transition: Who’s leading the shift?

The pace at which India’s data center industry is evolving is striking, not just in terms of capacity, but in the way sustainability and renewable integration are becoming central to the business models of key players.

Major investments and announcements include:

- AdaniConneX – Hyperscale, Sustainability-linked Financing (Source: DCD)

- What: AdaniConneX (Adani Enterprises and EdgeConneX) aims to provide 1 GW of data center capacity in India in the coming years.

- Finance/commitment: They announced a sustainability-linked construction financing framework with an initial commitment of USD $875M, which could expand to $1.44B. This financing will help accelerate development under ESG-linked terms.

- Impact: This puts AdaniConneX in a position to build hyperscale campuses with several alternatives for large-scale power procurement options and specialized renewable energy sources, supporting big expenditures in cloud and AI.

- CtrlS – Captive Solar Farm (GreenVolt 1) Powering Mumbai Campus (Source: DCD)

- What: 125 MW of power will be produced by the GreenVolt 1 solar farm close to Nagpur (two phases: – 65.2 MW launched June 2024; additional – 62.5 MW completed). The CtrlS campus in Mumbai will be powered by electricity from the farm.

- Investment/Scope: The project, which is over 340 acres in size, now provides more than 30% of the campus’s energy during Phase 1 and will increase to 60% in Phase 2. CtrlS is also investing in greenfield facilities (e.g., recent ₹500 crore investment announcements).

- Impact: This initiative greatly reduces Scope 2 emissions at the Mumbai campus, reduces grid and diesel dependency, and serves as a model for clean energy on large campuses.

- Nxtra (Airtel) – Large PPAs and Net-zero Target (Source: Developing Telecoms)

- What/Commitment: Nxtra has publicly committed to net-zero operations by 2031 and is actively procuring long-term renewable supply.

- PPA/Volumes: Announced long-term PPA agreements to procure – 140,208 MWh of renewable energy (multi-year agreements) to power its data-center portfolio.

- Impact: Demonstrates hyperscaler/telecom-backed operators using long-dated PPAs to match consumption and to de-risk energy price/availability while meeting ESG commitments.

- Equinix – First Captive PPA in India with CleanMax (26.4 MW solar + 6.6 MW wind = 33 MW) (Source: Equinix)

- What: Equinix signed a 33 MW captive renewable PPA with CleanMax (26.4 MWp solar & 6.6 MW wind) to serve its Mumbai data-centers; phase operational in 2025.

- Impact: Equinix’s move shows global hyperscalers bringing their decarbonization playbooks into India via captive projects and PPAs, an important market signal for local renewables developers.

These initiatives signal a strategic pivot, from treating power as a cost factor to viewing it as a core pillar of competitive differentiation. Energy sustainability is becoming part of the brand identity for next-generation data centers.

The Market Imperative: Energy, Investment, and ESG

The integration of renewable energy into data centers isn’t just about sustainability; it’s about market positioning and investor confidence.

In terms of energy consumption, investment, and sustainability, India’s data center sector is at a critical juncture. The industry anticipates $20 to $25 billion in investments and 4,500 MW of capacity by 2030. Developing digital systems that adhere to environmental, social, and governance (ESG) criteria is becoming more and more crucial. In its development plans, operators increasingly incorporate renewable power purchase agreements, sustainable funding, and green design criteria. A major change has occurred since energy efficiency and ESG compliance are now essential market standards.

By keeping an eye on emerging investment patterns, developments in green technology, and ESG-related possibilities throughout the data center value chain, Stellarix assists enterprises in managing this transition. Stakeholders can connect strategic growth with sustainability objectives and energy dependability from our insights. This guarantees competitive and ecologically sustainable growth.

The Global Context: Learning from Leaders

The data center industry is becoming more efficient and is increasingly using renewable energy around the world. Regions like the Nordics, Singapore, and Ireland demonstrate how data infrastructure can be developed sustainably. In 2020, Singapore changed its green permitting rules and paused new data center construction. This encouraged operators to adopt modern cooling methods and low-carbon designs. Nordic countries have taken the lead in creating net-zero data campuses by harnessing plentiful hydro and wind power for clean electricity and natural cooling. At the same time, companies like Google, Amazon, and Microsoft are aiming for 24/7 carbon-free energy in the US and Western Europe. They are achieving this by combining flexible grid solutions, battery storage, and renewable energy purchase agreements.

- Singapore, facing land and power constraints, temporarily paused new data center approvals until operators show their commitment to green sourcing.

- Denmark and Sweden are encouraging the use of waste heat, where excess heat from data centers goes to urban heating networks.

- The UAE and Saudi Arabia are connecting data centers with large solar parks and looking into integrating green hydrogen for base load power.

These examples serve as a guide for India. They emphasize climate-friendly financing, policy coordination, and energy localization as crucial elements for sustainable growth. Indian developers and policymakers can avoid the energy-intensive problems associated with rapid digitalization by examining these existing systems. Additionally, this information can expedite their transition to renewable energy.

Future Outlook: Building the Next-Generation Data Infrastructure

The next stage of growth will concentrate on energy and digital connection innovation as India’s data center ecosystem expands. In order to achieve efficiency and sustainability, future-ready data centers will integrate smart grids, use AI for energy optimization, install hydrogen-based backup systems, and apply cutting-edge thermal management technologies. AI-driven demand forecasting, on-site renewable microgrids, and liquid and immersion cooling will transform operating standards and reduce carbon emissions and energy consumption.

- AI for Energy Optimization: Predictive analytics is used to modify data loads according to grid conditions.

- Direct-to-Chip Liquid Cooling: Upto 40% less energy is used

- Microgrids and Peer-to-Peer Energy Trading: Allowing campuses to directly trade renewable energy.

- Green Hydrogen Backup Systems: Using hydrogen fuel cells in place of diesel generators.

- Circular Data Center Design: Repurposing waste water and heat for other industrial uses.

At Stellarix, we see this emerging frontier as a landscape rich with opportunity, where innovation scouting, technology intelligence, and partnership mapping can accelerate the shift toward smarter, cleaner, and more resilient digital infrastructure. By analyzing advancements in green computing, distributed energy systems, and sustainable design technologies, Stellarix helps stakeholders anticipate disruption and harness innovation to build a truly sustainable digital future for India.

Conclusion

India’s data center boom drives its digital future. It supports everything from financial inclusion to AI innovation. However, this growth needs to be powered wisely.

If renewable energy expansion keeps up, India could set a new standard for green digital growth and become a global leader in sustainable infrastructure. If it fails to do so, the country risks creating a digital economy that is carbon-intensive, strained on the grid, and environmentally weak.

The balance between data and energy (bytes and watts), cloud and carbon, will shape India’s future. This will determine its role not only as a digital powerhouse but also as a nation that chooses to grow responsibly.

In the age of intelligence and information, energy is the true backbone of progress, and sustainability is its guiding principle. With its strategic intelligence and analytical support, Stellarix is helping companies align carbon, cloud, and capacity to bridge the gap between data growth and sustainable energy.

Let's Take the Conversation Forward

Reach out to Stellarix experts for tailored solutions to streamline your operations and achieve

measurable business excellence.