Plastics is an umbrella term we often use disparagingly for all our inexorable polymers use. With already noxious levels of plastic pollution, 350 million metric tons more plastic waste reaches landfills and oceans yearly. As the world is on the edge of its non-biodegradable problem, global economies are pushing their teams to develop sustainable materials for plastics, enacting EPR rules, and making recycling a core part of the circular economy mix. With new-age plastic recycling management equipped with AI and blockchain, we can prevent a major possible human annihilation caused by one billion metric tons of plastic debris.

Thermoplastics – Reduce & Recycle

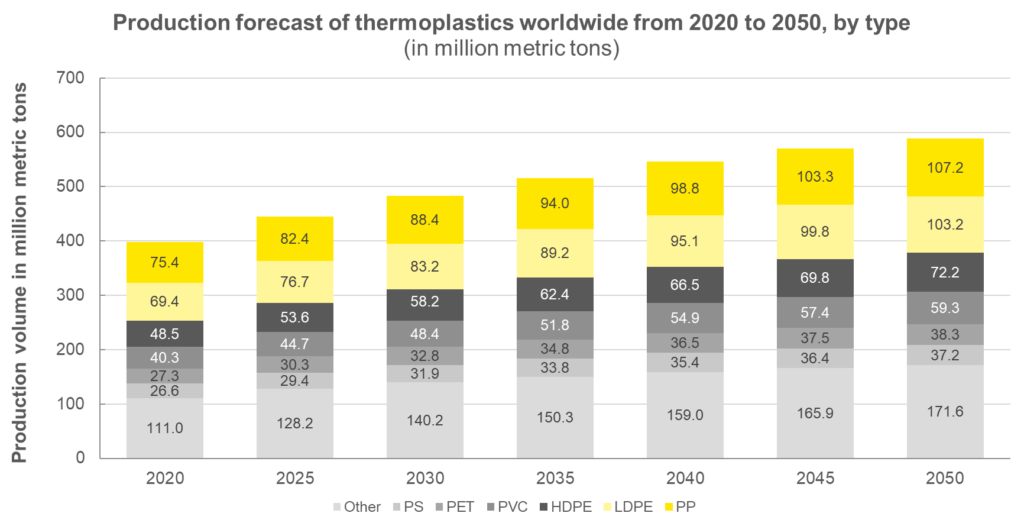

In the 1860s, scientists created the first artificial plastic, celluloid. However, as we fast forward to 1960, plastic started to become a problem. Scientists see plastic pollution in the ocean, with Laysan albatrosses swallowing plastic items and northern fur seals entangled in nets. Six key types of commodity plastic, namely polyethylene terephthalate (PET), high-density polyethylene (HDPE or PE-HD), polyvinyl chloride (PVC or V), low-density polyethylene (LDPE or PE-LD), polypropylene (PP), polystyrene (PS) comprise 70% of the global plastic production among which PVC, LPDE (single-use plastics) and PS being the least sustainable and toxic. Despite the significant health and climate damage caused by commodity plastics, analysts project growth in the global thermoplastics market from 445.25 million metric tons in 2025 to 589.03 million metric tons in 2027.

Reducing use, lowering production and recycling of thermoplastics are areas where countries are keenly working towards their Sustainable Development Goals under the Paris Agreement, a significant legally binding international treaty on climate change.

Figure 1: Production forecast of thermoplastics

Engineering Plastics

According to Stellarix’s adept research, high-performing and robust plastics, known as ‘engineered plastics,’ reached a value of USD $98.0 billion in 2022. They are projected to surpass $132.39 billion by 2027, with a compound annual growth rate (CAGR) exceeding 6%. The most common engineering plastic in pharma is polyethylene (HDPE/LDPE), which is used to make solid pharmaceutical products and create moisture-resistant and structurally rigid containers.

The automotive, electronics, and telecommunications industries commonly use acrylonitrile butadiene styrene (ABS) and polypropylene plastics. Consumers must educate themselves about plastic materials so they don’t get greenwashed. A genuine manufacturer is responsible for developing high-end products that mitigate environmental damage. The European Commission’s Waste Electrical and Electronic Directive (WEEE) requires the separate collection and proper treatment of WEEE by setting targets for E-waste collection, recovery, and recycling.

The Link Between Plastic Demand & Oil Growth

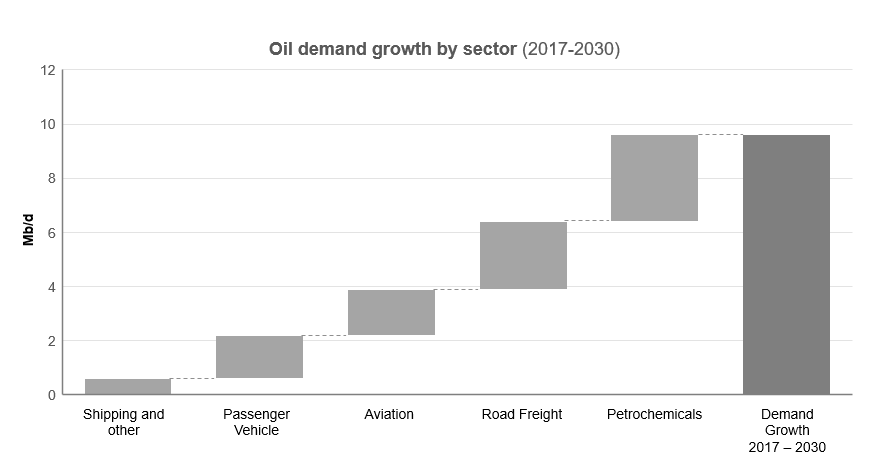

Non-biodegradable plastics are low-cost to manufacture due to petrochemicals/hydrocarbons such as naphtha, ethane, and Olefins derived/fractions of coal, natural gas, petroleum, and crude oil. Increased demand for plastics is invariably becoming a massive growth factor for oil demand and will account for nearly half of oil growth by 2050. Plastics from petrochemicals release CO2, a prime greenhouse gas leading to further climate change. Countries must reduce their dependence on low-cost plastics manufactured from petrochemicals for a truly circular economy.

Figure 2: Oil Demand Growth by Sector

Circular Economy as the Deliverer

From the 2019 Arctic Ice melting, termed as an ‘irreversible ice collapse’ to losing our biodiversity at a wretched rate, we only have ‘Circular Economy (CE) as our collective resolve against global climate crises and severe weather phenomena.

Industrial development and Information Technology 4.0 were linear in approach and impact, and with the all-encompassing climate change crisis, our way of working and thinking requires a full-circle approach. Moreover, a circular economy is best for establishing a long-term sustainable economy. It prioritizes environment-friendly inputs, the extension of product lifecycles, recycling and reuse, responsible utilization of shared resources, and the concept of product as a service. In the context of plastics, this approach takes into consideration the complete end-of-life of a product.

To achieve sustainability thresholds, stakeholders must actively direct their efforts towards addressing the nine planetary boundaries framework. These include climate change, ocean acidification, changes in biosphere integrity, the nitrogen and phosphorus cycles, atmospheric aerosol loading, freshwater use, stratospheric ozone depletion, and land-system change. By focusing on these areas, we can work towards creating a more sustainable future. Moreover, the circular economy will help prioritize systemic solutions via concepts like use less, use longer, use again, and make clean. This will improve our current 7.2 % circularity metric of material inputs.

Hold-ups in the Path of Circular Economy

Thus far, real progress in a circular economy is quite latent, with the EU’s recycling rate falling in 2020 and gaining only a 3% circularity rate for fossil energy materials, including plastics and fossil fuels.

As different plastic types require different recycling methods, the industry/sector must establish a centralized procedure for collecting similar plastic types for recycling. Most plastic waste is collected mechanically, and a large part is non-degradable. Currently, only 1% of bioplastics is being produced globally.

We can’t mix bioplastics with fossil-based traditional plastics, so there is a great need to create a proper supply chain and recycling system for new-age bioplastics.

In addition, biodegradable plastic waste requires certain prevailing environmental conditions to decompose fully naturally, and the absence of these conditions makes it part of the linear economy. Polylactic acid-based industrial compostable plastics require different handling as they decompose under industrial composting processes. Moreover, there is a strong need for materials R& D, procedure planning, tech advancement, and collaboration between key partners in the plastic manufacturing sector.

Latest Plastics’ Feedstock & Other Key Developments

To remain in a safe operating space (SOS) and not cross the threshold of the global surface temperature of 2°C, we have to reduce our carbon emissions, detrimental water usage, nitrogen fertilizer use, and unwarranted land utilization. There have been many breakthroughs in manufacturing plastics away from fossil fuels. Manufacturers are now making plastics from starch, protein, cellulose, sugarcane, and other bio-feedstock. Bioplastics use biodegradable materials such as corn starch and mix it with naturally putrefiable polyesters.

Protein-based biodegradable plastics use wheat gluten, casein, and milk. Moreover, other bioplastics, including aliphatic polyesters and even bio-derived polyethylene, are currently being explored. Researchers are exploring new catalyst technologies to enable carbon capture and utilization (CCU). They are also investigating process techniques and energy-saving methods as alternative approaches for recycling significant amounts of CO2 emitted by industries.

The chemical processing of plastic waste through pyrolysis is gaining traction, enabling the recycling of even the difficult-to-recycle waste. Like in the U.S., materials recovery facilities (MRFs) process plastics and materials through single-stream or dual-stream collections. Also, dual-stream collection involves recycling from two different feedstocks: one based on paper and the other consisting of glass, metal, and plastics. Researchers and innovators are developing various advancements to enhance the sorting of mixed plastic waste. Moreover, these include developing photoluminescent labeling, utilizing AI, incorporating near-infrared (NIR) detectors to identify chemical bonds in polymers, and implementing optical systems equipped with robot arms to effectively separate different types of plastics. In addition, these technologies will catalyze the circular economy by improving the sorting of different plastics and recycling outputs.

Circular Economy of Plastics: Packaging Industry & EPR Developments

European Union USA, among others, is working towards creating revised directives to minimize packaging waste and setting recycling targets/limits for manufacturers. European Commission has set new targets for recycling under the Packaging and Packaging Waste Directive (PPWD) to achieve 65% recycling for all ‘packaging waste’ and 50% recycling for ‘plastics’ by December 2025. Further, the UK has updated its extended producer responsibility (EPR) regulations for packaging for businesses supplying over 25 tons of packaging in a year. Also, it is liable for EPR fees and additional modulated fees based on recyclability and label requirements expected to be implemented in 2025.

Packaging producers and importers will need to provide packaging recovery notes (PRN). In addition, these PRNs will serve as proof of recycling, recovery, or exportation of one tonne of packaging. Similarly, the EU’s plastic strategy aims to create an Extended Producer Responsibility (EPR) scheme. Also, this scheme will enable producers/suppliers to keep tabs on the kind of plastics that enter the EU market. EU’s EPR systems/directives would encourage producers to improve their recycling efficiency, make products designed for recycling, reduce plastic waste/carbon emissions, and increase dialogue between producers, local authorities, and recyclers.

Conclusion

Plastic recycling is inevitable in the future, yet we can 100% increase plastic recycling. Circular solutions are increasingly becoming the focus of all key industries. These industries include agrifood, manufactured goods & consumables, mobility & transport, and the built environment. Moreover, most countries are at different stages in their sustainable goals, and every country needs to learn and support each other. Also, with countries, businesses, and people’s greater resolve to solve the present complicated climate change hurdle, they need stronger resilience, creativity, and resourcefulness. In addition, more polymer research, recycling infrastructure, increased manufacturer’s responsibility (EPR), and global/local action is a must to sort out the world’s toxic plastic headache.