Automotive Supply Chains Under Siege: How Disruption is Rewriting Value in the US and Europe

Key Takeaways:

- The automotive trade network is heavily concentrated, with five hubs controlling 75% of global EV trade. This structure can handle random disruptions, but targeted intervention against core hubs like China and Germany would expose its deep-rooted vulnerabilities.

- Geopolitical factors have become the dominant source of supply chain risk, surpassing demand fluctuations and natural calamities. Vehicle assembly, along with battery production and raw material extraction, is a highly susceptible area across the mobility value chain.

- The US faces persistent gaps in mid-stage manufacturing capacity despite IRA policy incentives, while Europe struggles with high energy costs and mounting competition from China. These distinct pressures make supply chain redesign mandatory.

- Value is shifting from mechanical hardware to software, where capabilities such as digital twins and data security distinguish resilient suppliers from those struggling to adapt.

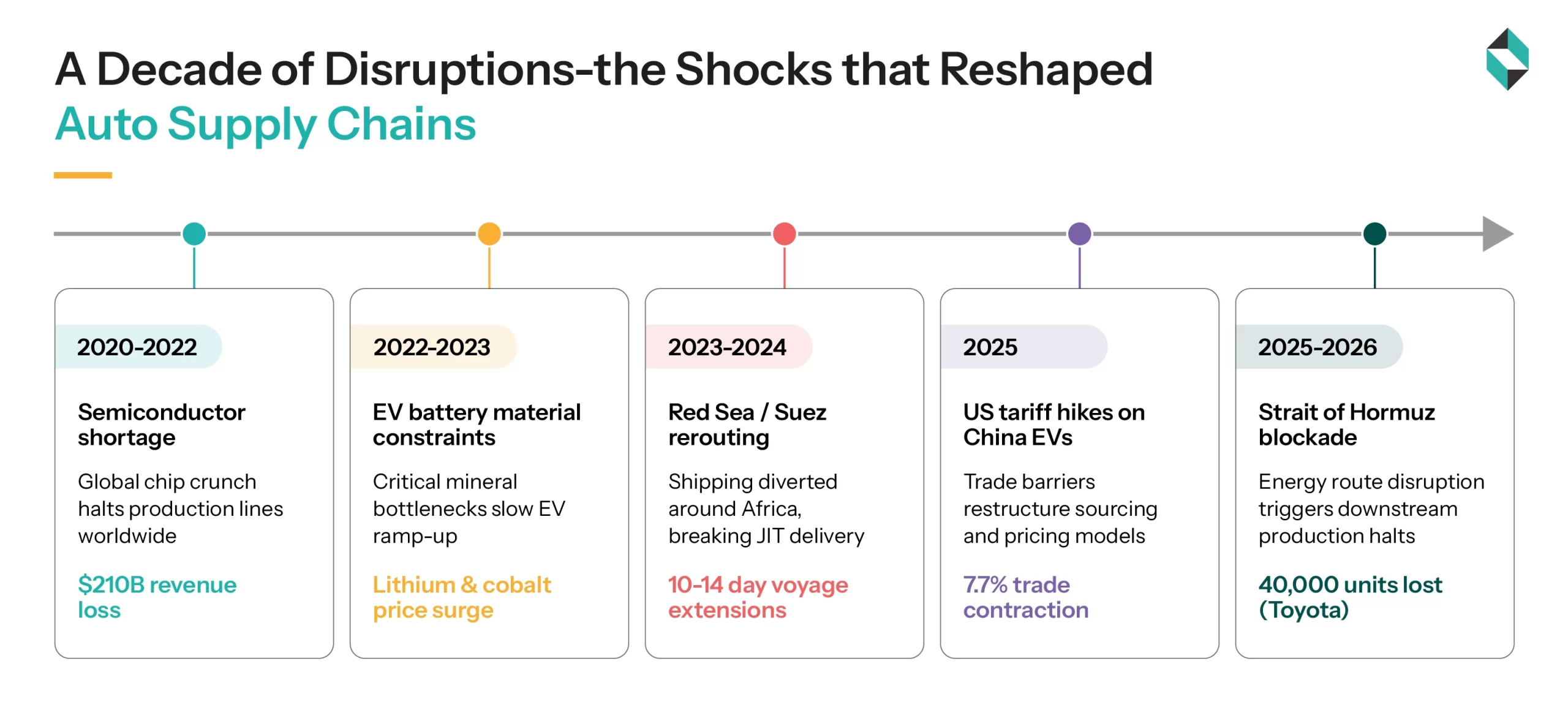

The automotive supply chain is currently undergoing the most volatile period, with the mobility sector being impacted the most. The sector is under severe strain from events ranging from pandemic-related semiconductor shortages to trade policies. Maritime chokepoint closures and raw material inflation have further intensified the crisis.

The EV network is dominated by five key hubs, which account for ~75% of trade globally. This supply chain structure is highly resilient to sudden market disruptions but remains extremely vulnerable to targeted interventions against China as well as Germany. A projected US tariff hike on Chinese EVs in 2024, around 7.7%, led to rapid restructuring of geopolitically aligned blocs, resulting in “friend-shoring”.

Geopolitical risks have heightened concern among industry players in recent years, particularly affecting lithium ore extraction and battery manufacturing, which are at highly vulnerable stages.

The impact of these shocks is evident in real-time cases like Toyota and Ford. Toyota reduced Middle East-spec Land Cruiser production by approximately 40,000 units due to supply chain disruptions caused by the Red Sea crisis, coupled with the Strait of Hormuz concerns. Such disruptions lead to delays of several hours, with most losses occurring not from failures but from response times.

The US Automotive Context

The Inflation Reduction Act (IRA) in the US triggered a surge in investment, leading to record levels of industrial spending and the emergence of new manufacturing clusters in the South and Midwest. However, the development of local battery manufacturing has been inconsistent along the entire value chain. Although cell and pack capacities are likely to meet demand, there will be notable shortages in midstream components such as cathodes, anodes, and separators, even assuming all domestic capacity plans are realized by 2030.

The auto tariffs imposed in 2025 on cross-border parts flows have further complicated the landscape. As a result of a closely integrated US-Canada-Mexico supply chain network, procurement teams are left with only two choices: either to absorb cost increases or to restructure logistics networks.

The US is largely dependent on a global supply chain network where China controls 70-90% of critical segments of the lithium-ion value chain. This dependency poses particular concentration risks while deepening the supply chain crisis. The 2025 confiscation incident at a nickel mine in Indonesia highlights challenges for automakers. This particular event triggered a price hike and put huge pressure on automakers that relied on those supplies.

Major automakers like Ford reported a $6 billion loss because of supply chain disruptions. General Motors also pointed to unpredictable logistics as the main reason for its lower profit margins. These examples show why the supply chain system needs a major redesign.

Attempts to remove federal EV tax credits and weaken state rules like California’s ACC II program have created economic challenges. These changes could sharply lower domestic battery demand and put existing cell manufacturing capacity at risk.

The European Automotive Context

The sector is confronting a fundamentally different crisis driven by rising localized energy prices and fierce competition from low-cost Chinese OEMs. Further, German suppliers are under significant margin pressure as the EU still relies heavily on Chinese battery materials despite the implementation of retroactive tariffs.

Europe’s legacy automakers are focusing on cost restructuring to deal with market competition and pressure. Volkswagen Group reported a 53% decline in its 2025 operating result to €8.9 billion, driven by trade barriers and restructuring costs. These challenges caused supply chain redesigning or process changes among firms with consideration of the closure of German plants.

Additionally, Stellantis announced a €22.2B investment by the end of 2025 and suspended its 2026 annual dividend to realign its product strategies in line with the changing pace of the European EV transition. Meanwhile, German Tier-1 and Tier-2 suppliers face a critical margin squeeze due to persistent power costs, leading to a sharp contraction in the regional supplier ecosystem.

To avoid EU auto tariffs, Chinese battery firms are shifting to local production, establishing Hungary as Europe’s leading battery manufacturing center. CATL’s €7.3 billion Gigafactory is increasing commercial output. This local supply chain is strategically important for BMW’s “Neue Klasse” platform as it uses CATL’s localized Gen6 cylindrical cells to minimize supply chain unpredictability.

To deal with cost pressure, VW and Stellantis have partnered with Chinese firms in manufacturing, autonomous driving, and R&D. Renault, despite no direct sales in China, established an R&D center in Shanghai, which helped halve the production time for its Twingo model to 21 months.

China’s leadership in battery manufacturing and its growing dominance in the lithium iron phosphate segment make up for 98% of production. Overall, it poses major competitive challenges for existing market players worldwide.

Further, the Chinese government introduced the New Energy Vehicle Promotion Policy (NEVPP) to alleviate financing difficulties and address supply chain vulnerabilities. Overall, it creates a model for a policy-driven, state-supported industrial ecosystem that European automakers must now compete with.

Where Value is Shifting?

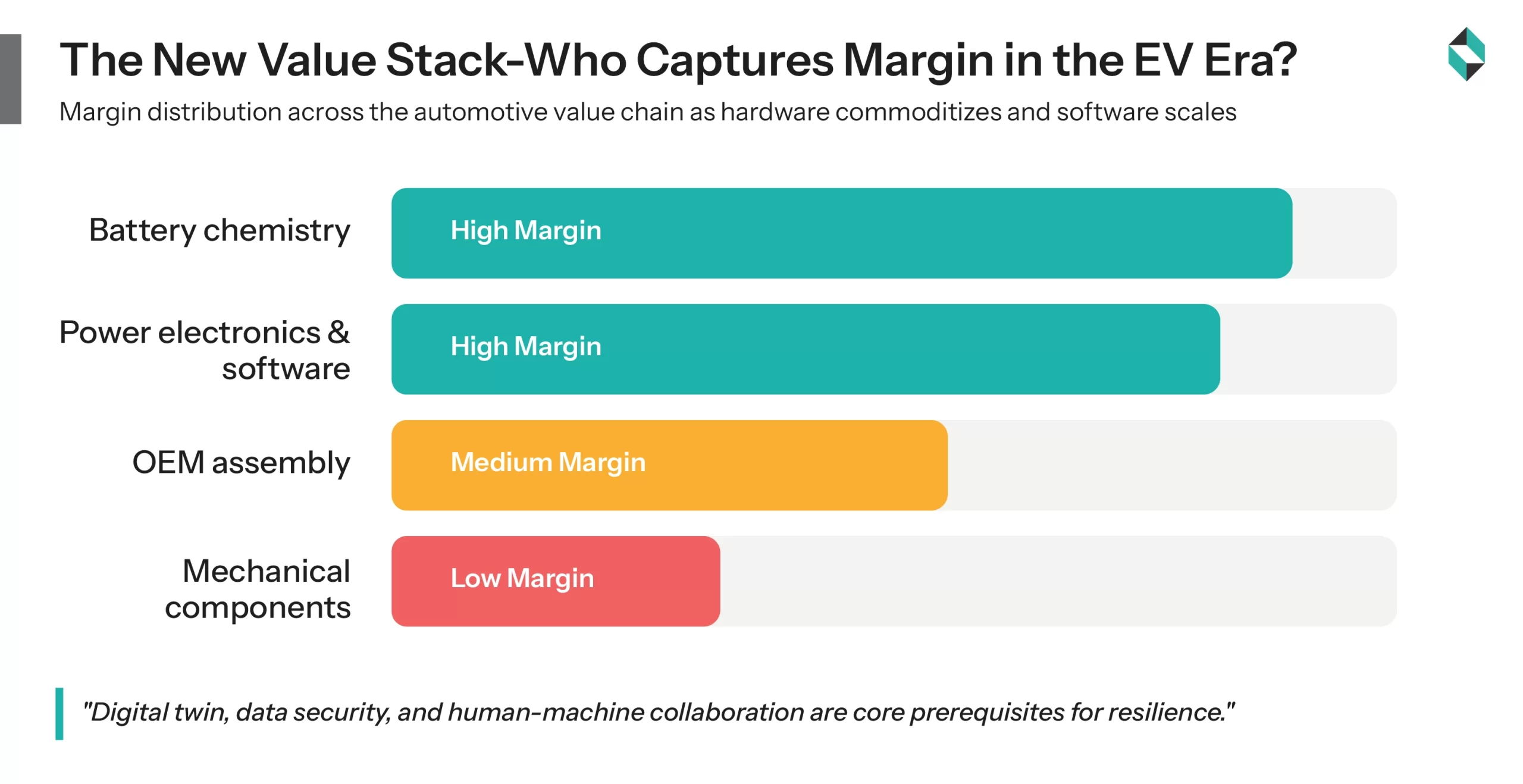

The shift to electric vehicles is fundamentally changing where economic value is generated. The focus is shifting from the mechanical complexity of internal combustion engines (ICEs) to EV software and battery chemistry. Studies on digital twin technology show that it enhances supply chain resilience by offering multiple effective configurations of its key attributes, rather than relying on a single approach. Key factors such as data security, human-machine collaboration, and digital twin applications consistently appear as essential requirements for supply chain robustness.

In the new value stack:

- OEMs aim to take control of software and user interfaces.

- Tier 1 suppliers are rushing to develop high-performance computing platforms.

- Battery manufacturers are capitalizing on supply shortages to command higher prices.

- Suppliers with key intellectual property in power electronics have gained influence, while those producing only mechanical parts face margin pressures.

Cumulatively, the design approach that connects product engineering, manufacturing, and sourcing is becoming more vital for managing value chain disruption.

Strategic Responses

Automotive leaders are focusing on proactive operational management strategies with a central focus on near and dual shoring. Mexico is emerging as a favored location due to its proximity to the US market. Also, vertical integration is making a comeback as OEMs explore developing their own battery manufacturing capabilities.

Digital supply chain control towers are tracking Tier 2 and Tier 3 nodes that address a longstanding bottleneck. Moreover, policy is increasingly common as a resilience strategy. Analyzing China’s NEVPP illustrates how policy can enhance resilience through financial and technological support.

For European and US automakers, it is necessary to mitigate sourcing restrictions arising from the EU Critical Raw Materials Act and the IRA to ensure market access.

Bottomline

The automotive supply chain underwent a decade of repeated shocks, revealing its underlying fragility. From semiconductor shortages during the pandemic to geopolitical tensions and rising tariffs, manufacturers have had to confront a structural vulnerability that globalization focused on efficiency had masked for years. Targeted tariffs significantly contribute to systemic risk and supply chain fragmentation, providing a solid basis for evaluating trade policies and developing resilient industrial strategies. As an innovation and strategy partner, Stellarix is working with industrial, automotive, and mobility leaders to turn supply chain fluctuations into operational resilience. Through our strategic foresight and market and business strategy consulting services, we support industry players from scenario planning and supply chain risk navigation to the identification of suitable co-man via strategic partner scouting.

Let's Take the Conversation Forward

Reach out to Stellarix experts for tailored solutions to streamline your operations and achieve

measurable business excellence.