Silent Disruption: The Expanding Market Share of Chinese OEMs in the Western Hemisphere

Executive Summary:

Chinese OEMs are currently holding a 25–35% cost-per-vehicle advantage over their Western counterparts. Apart from vertical integration, their native software architecture and LFP battery chemistries have been the key drivers of their success halfway across the world. Even though Europe tried to slow down its pace with countervailing duties, the maneuver only accelerated its local manufacturing drive in Spain and Hungary. Moreover, the most puzzling factor is the increasing reliance of European and US battery and SDV manufacturers on Chinese supply chains. This paradox is driving the tension in the West as the dragons from the East rise at an unprecedented pace.

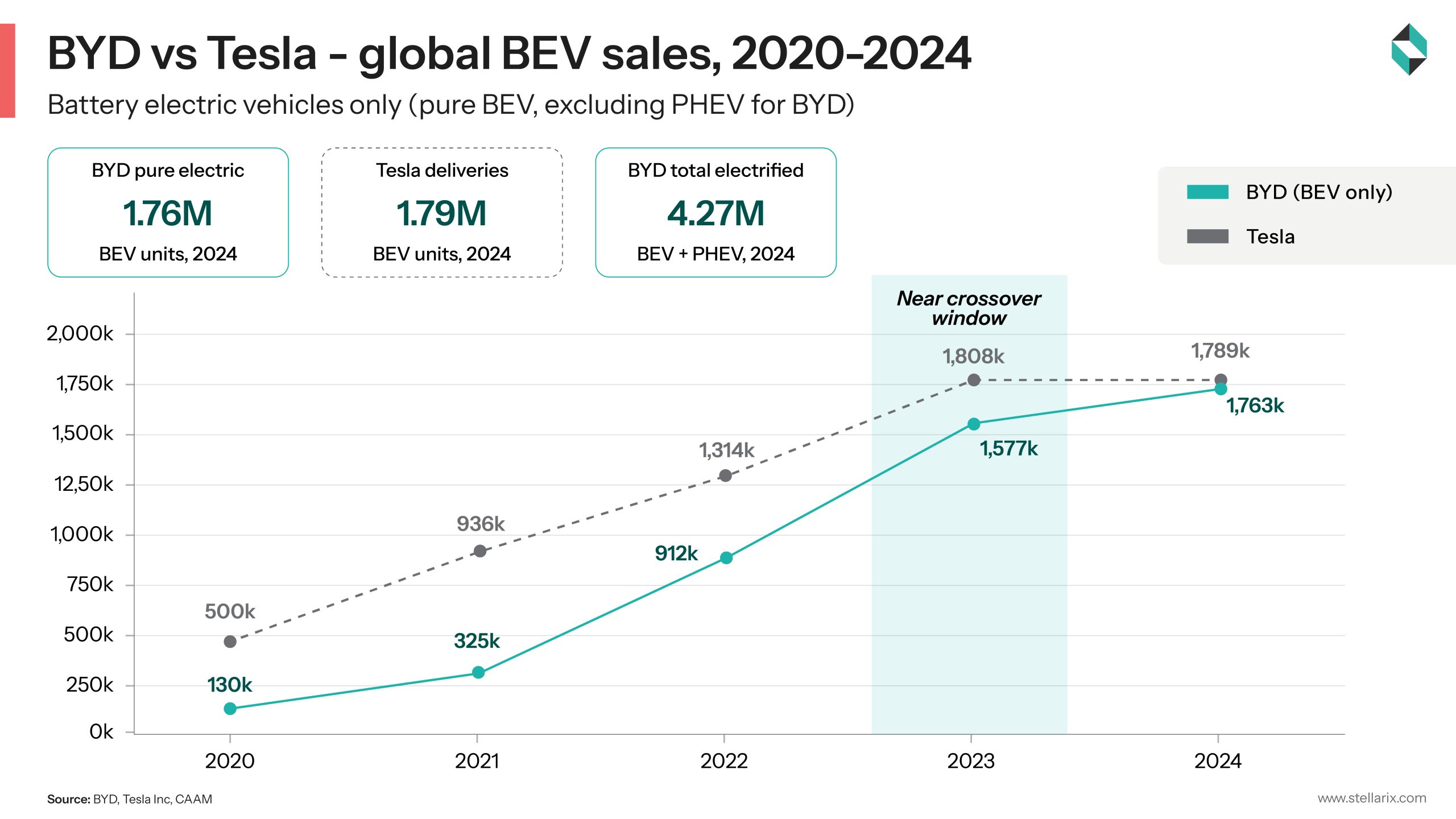

For the better part of the last half-decade, the Western Hemisphere was busy navigating the supply chain crisis first caused by the pandemic and then other geopolitical disruptions. On the other hand, their Chinese counterparts were developing something very, very different – a vertically integrated, software-first automotive ecosystem to cater to the moment that this industry is standing at right now. Their entry and expansion in the European and American markets break their assumption that they are formidable within their domestic market. The most evident development that confirms this is that BYD surpassed Tesla in 2024 to become the largest seller of plug-in hybrid and battery electric vehicles by volume. Also, China’s dominance in global semiconductor manufacturing is now increasing the reliance of the SDV segment on it, becoming a bigger challenge for market leaders like Nvidia.

It’s a structural market shift, one encouraged by supply chain complications and a decade of strategic investment policy in China. However, to understand this shift, a closer look at the mechanism is required, not just at the numbers.

It’s Time to Acknowledge: Structural Cost and Tech Advantages are Developed, not Borrowed

The upper hand that Chinese OEMs hold in the West is not just a product of currency manipulation or cost-effective labor, but the speed of systemic vertical integration execution that surpassed the capabilities of their Western counterparts.

BYD sets a clear example of it. It is manufacturing its own lithium iron phosphate (LFP) batteries, electric motors, semiconductors, and software stack. The cost consequences have been substantial. As per BYD’s 2024 cost-per-vehicle cost analysis, this self-reliance helped them reduce per-vehicle cost by 25-35%. This gap widens further due to supply chain disruptions, the ongoing Hormuz lock, and growing reliance on nickel and cobalt for European and American OEMs.

Similarly, CATL, the dominant battery cell manufacturer, is currently sitting at the center of the Chinese OEM ecosystem. Its proximity to the Chinese automotive players gives them a supply priority, battery pricing, and technical co-development access leverage. Perks that Western CATL clients do not get. Overall, the supply chain that European companies currently hold for their electrification is partially owned and marginally aligned with their Chinese competitors.

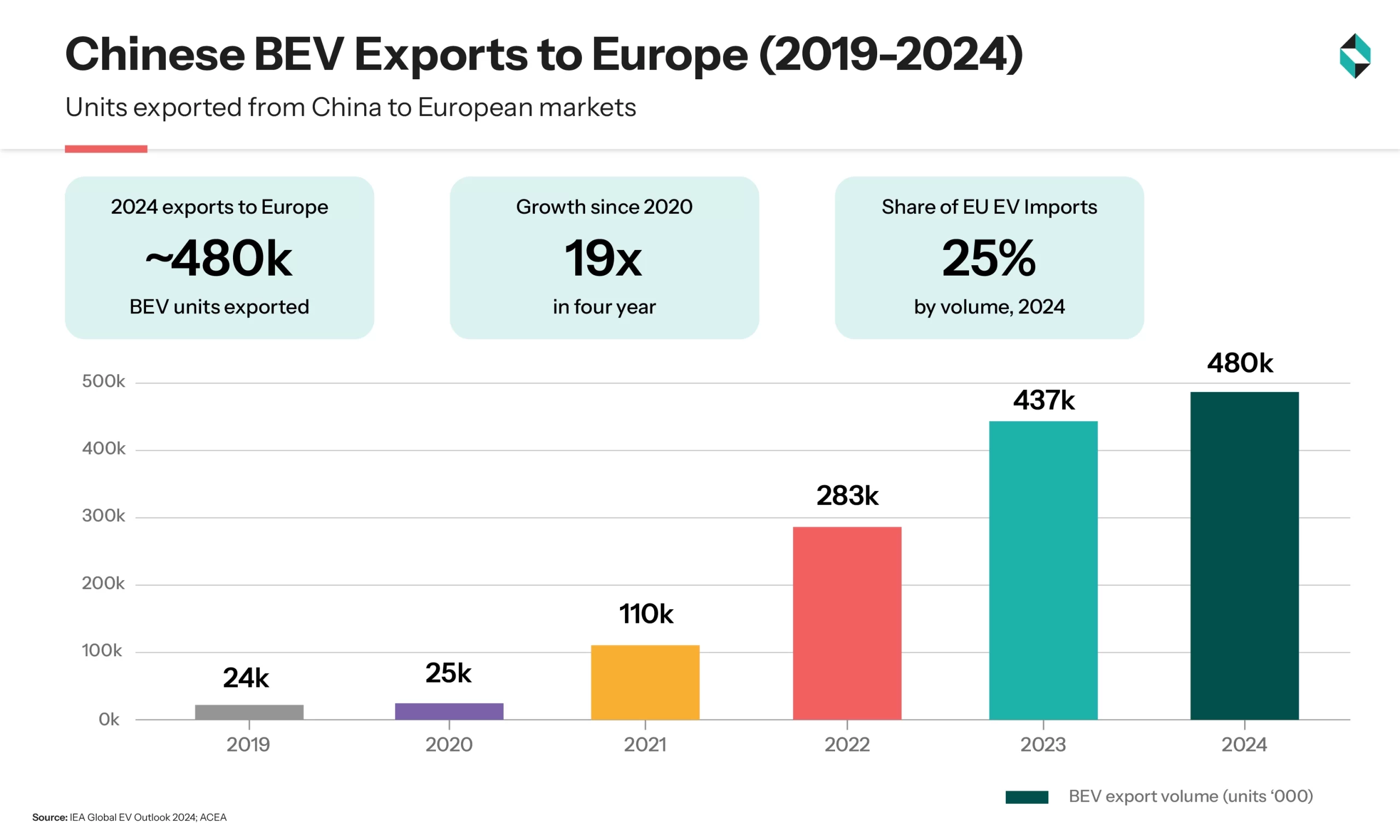

Key Metric: The average selling price of a normal Chinese EV exported to European markets in 2024 was roughly €32, 000. A figure that was approximately €10,000 – €15, 000 less compared to Renault, Stellantis, and Volkswagen equivalents.

Beyond cost, the SDV architecture adopted by Chinese OEMs from their pioneers allows them to hold an upper hand in product experience. This works in their favor in markets where new buyers evaluate vehicles by their digital interfaces along with drivetrains. OTA updates, AI-assisted driver systems, and deeply integrated infotainment are now native to vehicle frameworks, and they are leading this aspect at a global scale.

Lastly, it is the Chinese regulatory support that is paving the path for their domination in this space. OEMs are getting subsidies for battery production, energy, and land at reasonable prices for EV production, and direct support for entry in overseas markets. However, none of these support measures stands against the genuine industrial capability of this nation, which will persist even with the lowest government support.

The European Paradox: Battle between Local Assemblies, Tariffs, and Increasing Chinese Parts Consumption

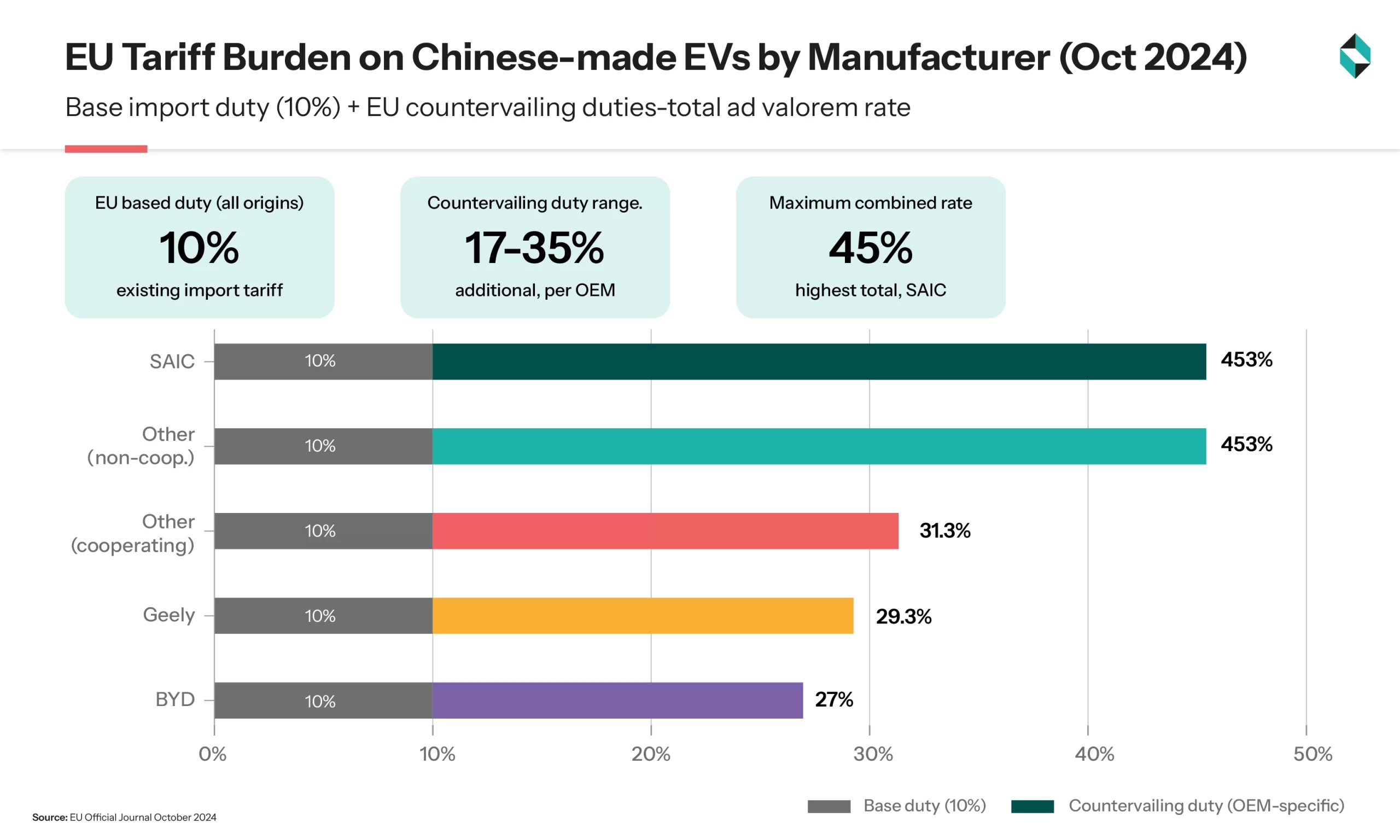

The EC responded to this expansion in 2024 with increased import tariffs. While BYD received an additional 17%, SAIC had 35%, and other manufacturers had an approximately 21% increment. However, this countermove didn’t dissuade the strategic push. BYD opened up a new plant in Hungary, which represents a calculated tariff bypass. It allows them to avoid import duties irrespective of the country of origin of components. SAIC went to explore partnerships in Central Europe. The pattern is clear; the tariff is being kept aside to accelerate localization.

On the other hand, the European OEM lobby represents a different paradox. While automakers are demanding tariff protection, they are buying components and batteries from Chinese companies.

Consumer reception in Europe has been more nuanced than early skepticism anticipated. MG, despite its Chinese ownership under SAIC, has leveraged its British heritage positioning effectively. BYD’s Atto 3 and Seal models received strong reviews from European automotive media. Price sensitivity in markets like Germany and France, where EV adoption incentives have been trimmed back, is creating space for value-positioned Chinese products that would not have existed two years ago.

America: Easy to Enter, but Tricky to Sustain in the Long Run

In the American subcontinent, the north remains closed to Chinese OEMs since Biden’s administration brought 100 percent duties on their EVs. Currently, the USA is an impenetrable policy fortress. South America, on the other hand, is another story. BYD recently opened its manufacturing facility in Brazil and turned the former Ford facility into an EV production site.

Brazil’s combination of a large addressable market, government EV incentives, and a relatively open trade framework turned it into an investment magnet. By the end of 2024, BYD held over 30% of Brazil’s electric vehicle market.

Chery has established assembly operations in Mexico, a market that sits inside the USMCA trade zone — a detail with significant strategic implications. While USMCA rules of origin provisions currently limit the ability to use Mexican-assembled Chinese vehicles to access US market tariff benefits, those provisions are subject to future negotiation. A manufacturing presence in Mexico creates optionality: the ability to pivot toward US market access if political and trade conditions shift, without having to build the capability from scratch.

Chile, Colombia, and Argentina are seeing rapid EV market share growth driven by Chinese models. In markets where grid parity economics are compelling, and Western OEMs have historically underserved the value segment, the Chinese competitive proposition lands with particular force.

Implications for European and American OEMs and Their Supply Chains

The entry of well-capitalized, cost-advantaged Chinese OEMs into Western markets is not simply a competitive threat to manage – it is a structural pressure that is forcing a reckoning with the economics of European and US automotive manufacturing.

The pricing compression is already visible. Stellantis, Renault, and Volkswagen have each announced restructuring programs with explicit reference to the need to compete with Chinese cost structures. VW’s 2024 announcement of potential German plant closures — the first in the company’s modern history – cited, among other factors, the need to achieve cost parity with new market entrants. The Chinese OEM challenge is functioning as an accelerant for industrial restructuring that was already overdue.

At the supply chain level, a bifurcation is beginning to emerge. Western OEMs are under political and regulatory pressure to localize supply chains — particularly for batteries — away from Chinese sources. At the same time, the most cost-competitive battery supply remains Chinese. This creates a dual-track procurement environment: compliant supply chains for incentive-eligible vehicles, and cost-optimized supply chains for everything else. Managing both simultaneously adds complexity and cost that Chinese OEMs, with their integrated domestic supply bases, do not face in the same way.

The strategic responses being explored vary in ambition. Some OEMs are pursuing co-opetition: GM’s long-standing SAIC joint venture in China, while under recalibration, reflects a model of engaging Chinese partners rather than purely competing with them. Others, including several European brands, are exploring technology licensing or platform partnerships with Chinese firms as a way of accessing cost-efficient EV architectures without the capital intensity of building them independently.

The cleanest competitive moat for western OEMs in this environment is not cost — it is brand, distribution depth, and regulatory familiarity. In the US, the regulatory fortress is real protection for now. In Europe, brand loyalty and dealer network depth still matter, though both are eroding faster in the EV segment than in ICE. In Latin America, there is limited structural protection, and the competitive window for Western OEMs to establish strong EV-era positions is narrowing.

Bottomline: It’s not Competitive but Strategic Clarity that Holds the Key

The Chinese OEM expansion into Western markets is not a passing trade friction or a tariff problem to be managed at the policy level. It is a lasting shift in where automotive capability and cost leadership reside. The organizations that will navigate it effectively are those that acknowledge the reality, with their boards, their investors, and their supply chain partners, about where their competitive advantages genuinely lie and where they do not.

For western OEMs, that means making deliberate choices: which segments to defend, which to cede, where to partner, and where to compete. Doing all things simultaneously is a daunting task.

For suppliers, it means assessing their exposure to OEM customers under margin pressure, and their opportunity to serve Chinese OEMs building local manufacturing footprints in Europe and Latin America, a customer set that is growing, not contracting. As a strategic partner, Stellarix is offering assistance to Tier-1 and Tier-2 suppliers, automotive OEMs, and mobility investors across the following interconnected practice areas:

- Partnership Strategy & Market Entry: Both European and Latin American incumbents face unusual complexity in partnership decisions. Our assistance is evaluating, structuring, and mapping potential engagement targets with a specific focus on value integration and operational clarity.

- R&D Strategy and Technology Positioning: The shift to new chemistries and SDV is a multi-layered set of investment decisions that need to be backed by competitive implications and payback horizons. We aren’t just helping with technology landscape mapping, but also with R&D investment roadmaps to navigate constrained capital budgets and accelerate development cycles.

- Market Intelligence and Competitive Manufacturing: The speed of Chinese expansion is outpacing the standard annual market reports’ ability to provide structurally adequate decision-making inputs. Our market intelligence is making up for that gap and is helping companies determine an apt response to market conditions.

Let's Take the Conversation Forward

Reach out to Stellarix experts for tailored solutions to streamline your operations and achieve

measurable business excellence.