Can Feedstock Alternatives Resolve The Crunch In Biofuel Industry?

Is the Feedstock Crunch Finally Here in 2026?

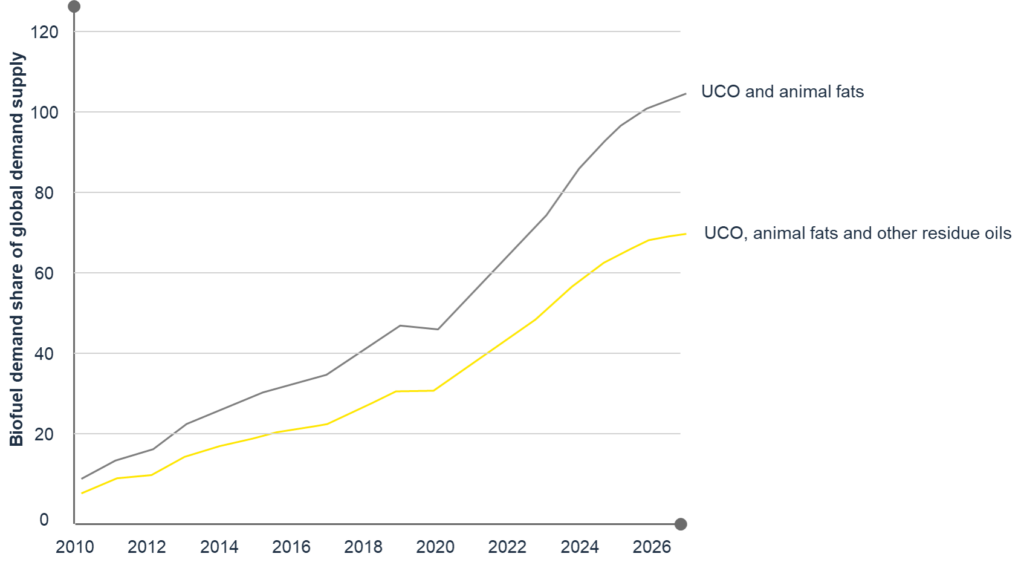

As per the latest IEA reports, the scarcity of feedstocks and waste-based oils is now a market reality and not a future threat. Feedstock demand will jump 70% from just over 25 million metric tons annually to more than 60 million metric tons by 2030 to meet announced blending targets. Also, the demand for waste and residue oils is projected to exhaust nearly 100% of the global supply by 2027.

The EU’s ReFuelEU Aviation mandate requires 2% sustainable aviation fuels (SAF) blending at EU airports, increasing to 6% by 2030 and 70% by 2050. The HEFA pathway, the most established SAF technology that uses used oils, faces structural input limitations because global estimates indicate that collectible fatty waste can meet only 3-4% of global SAF demand by 2050. This mandate is boosting demand beyond the current waste-based supply.

For more on SAF advancements and challenges, read our blog- Sustainable Aviation Fuel: Advancements and Challenges

If the producers stick to their old patterns without finding sustainable alternative sources of biofuels, the problem will become huge. The demand for feedstock alternatives like residue and waste-based biofuel is exceptionally high. It helps manufacturers meet the tightening emission regulations and feedstock policy objectives. Overconsumption of this feedstock creates a big vacuum for livestock feed supply, pushing food prices up directly and indirectly.

Also, the problem is rooted deeper in the appropriation of agricultural land in feedstock production, with increased fertilizer and pesticide usage that disturbs the long-term sustainability and organic food production goals. This precarious scenario calls for better feedstock alternatives and regulatory support. Moreover, identification of unsustainable and fraudulent waste supplies. The Global Bioenergy Partnership report estimates that biofuels will meet approx 27% of global transportation fuel demand by 2050, mandating the need for strong acknowledgment and resolution of these challenges.

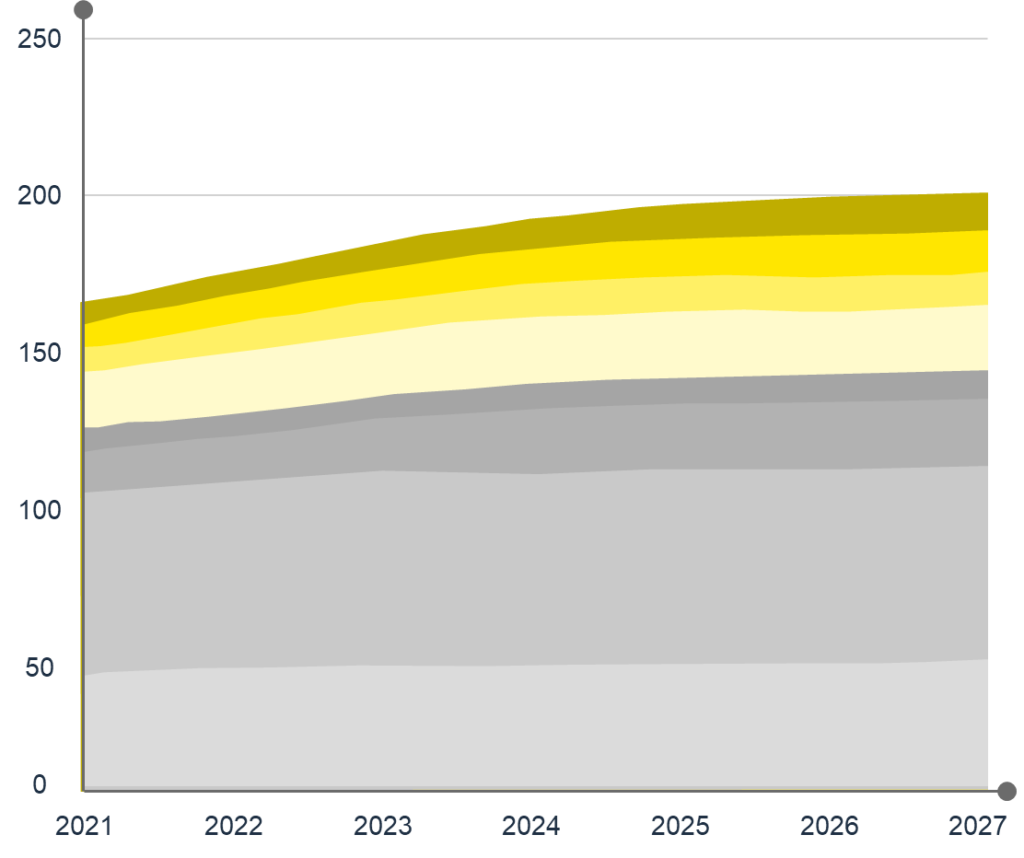

Figure 1: Total Biofuel Production By Feedstock From 2021 – 2027(E) (Source: IEA)

Biggest Challenges in Feedstock Alternative

First Generation Feedstock

The first-generation feedstock comprises the most abundantly available raw materials, including starch-based and sugar-based feedstock, potato, wheat, barley, sugarcane, and sugar beet plants. The pandemic, followed by the Russia-Ukraine crisis, has disturbed supply chains and grain distribution across the globe. Russia and Ukraine are the world’s first and fifth-largest wheat producers. Europe’s ongoing conflict and energy crisis have intensified food inflation and threatened food supplies. It has happened especially in Asia, Africa, and South America. This adds extra pressure on the US and Europe to produce more land to meet this looming demand. Moreover, the stress of offering less land to biofuel feedstock mounts. As food takes priority over fuel for more than half of the world, Western governments have pressure to shift to second-generation feedstock and curb the grain shortage.

Second Generation (2G) Feedstock

The second-generation feedstock has been developed to combat the first-generation feedstock’s food vs. energy dynamic. It comprises lignocellulose or carbohydrate biomass, a potent substitute for first-generation counterparts. However, the issue lies in the complications related to logistics, production costs, and complexity compared to their predecessors.

The International Renewable Energy Agency (IRENA) report states that the production cost of second-generation feedstock is 2-3 times higher than that of first-generation biofuels. The capital costs, land use conflicts, infrastructure limitations, and transportation are obstacles to successfully deploying and implementing these biofuels. Cellulosic ethanol production involves complex processes, such as biomass pretreatment, enzymatic hydrolysis, and fermentation. Developing efficient and cost-effective technologies for each step remains a significant challenge. Achieving high conversion rates and optimizing the enzymatic processes to break down the complex lignocellulosic structure of biomass efficiently is a technological hurdle that needs to be overcome.

Ensuring a reliable and sustainable biomass feedstock supply for second-generation ethanol production is critical. Obtaining a consistent and economically viable feedstock supply can be challenging due to factors like seasonal variations, geographical constraints, and competition with other uses such as animal feed and bioenergy. The bulky biomass feedstocks’ collection, transportation, and storage also pose logistical challenges. The public’s perception and acceptance of second-generation ethanol can impact its market adoption. Demonstrating the sustainability and positive environmental benefits of this alternative feedstock-based ethanol can help build public trust and acceptance.

Third-Generation Feedstock

The third-generation feedstock comes from algal biomass and waste oil. It neutralizes all the challenges of the first two-generation biofuels but comes with problems. IEA reports that the production costs of algae-based biofuels are approx $7 per liter. The first-gen biofuels cost more than $0.5 – $1.5. Then there is the issue of scaling up production and huge water and nutritional requirements that may involve negative environmental repercussions in the long run. For instance, the US Department of Energy states that algae cultivation may range between 1000- 2000 gallons of water for every 1000-2000 gallons of fuel production. Lastly, a National Renewable Energy Laboratory report states that large-scale algae cultivation for biofuel production may lead to nutrient pollution and habitat destruction. Therefore, through utmost care and responsibility, the path to implementation can take place.

| Feedstock | 2025 Trend | 2026 Driver |

| Used Cooking Oil (UCO) | Extreme Volatility | EU SAF mandates (2% in 2025 to 6% by 2030); competition with road biodiesel |

| Soybean Oil | Demand Surge: Transitioned from a food commodity to a primary energy feedstock. | The “One Big Beautiful Bill Act” (2026) in the US has reduced the tax-credit gap between waste oils and virgin oils, stabilizing its role in SAF. |

| Animal Fats (Tallow) | Steady Appreciation | Heavy bidding wars between Renewable Diesel (RD) and SAF producers for high-lipid-density waste. |

| Agricultural Residues | Industrial Scaling | Infrastructure maturity & policy support like India’s JI-VAN Yojana and EU RED III Annex IX incentives |

IEA analysis indicates that the primary obstacle for biodiesel is feedstock scarcity. Currently, biodiesel production capacity exceeds 2 billion liters annually, but this is only a small portion of the amount required to achieve government goals.

Furthermore, the IEA suggested implementing guaranteed pricing models for UCO-based biofuels, similar to successful ethanol pricing methods, to increase demand and support third-party aggregator networks.

2026 SAF mandates are increasing competition for limited waste-based feedstocks, with the identified shortage of fats, oils, and greases as a key obstacle to scaling biodiesel and SAF production.

The Solution in Feedstock

Better Technology Deployment

Technological stagnation is a subtextual demand concerning second and third-generation biofuel production. In the current scenario where the world struggles to feed all mouths while keeping air, water, and land clean and clear, delving a little deeper to find technological solutions is crucial. Waste animal fats and used cooking oil offer many non-food crop feedstocks for renewable biofuels. Therefore, better technical backup can upscale and economize non-food-based biofuel production. For example, biomass-based Fischer-Tropsch and cellulosic ethanol-based technologies can employ alternative feedstocks for biofuels to yield low-carbon biofuels for commuting and transportation.

Feedstock Innovation Spotlight 2026

Several production modus operandi have up-scaled the production of biofuels on a commercial level. However, a big innovation gap exists in converting grass or wood-based biomass into liquid biofuels. Thermochemical processes like bio-FT synthesis, rapid pyrolysis, and hydrothermal gasification can help fill this gap. However, the second-generation (2G) biofuel market has moved decisively from R&D to commercial scaling.

- Carinata and Camelina: These winter oilseed crops, along with pennycress, are defining 2G feedstocks for 2026 as they can be grown and nurtured on marginal lands, bypassing the fuel vs fuel discussion. It is estimated that these crops can produce around 4.24 billion liters of SAF annually by 2048, at a cost of $0.68/liter of bio-oil at the biorefinery gate, with meal credits reducing overall expenditure by up to 70%.

- Scientific validation of Municipal Solid Waste (MSW): Transforming MSW into SAF through processes such as Fischer-Tropsch synthesis and gasification can reduce GHG intensity by ~90% compared with traditional jet fuels.

- Cellulosic Ethanol: It is a vital solution to the widespread issue of feedstock shortages, with global capacity under development reaching a record 470,000 tonnes per year. This nearly doubles existing operational capacity, indicating a shift toward non-food sources like agricultural residues. Brazil is at the forefront of this industrial growth, recently establishing a facility that processes 62,000 tonnes of sugarcane bagasse annually. In addition, India launched Asia’s first 2G Ethanol Biorefinery in Panipat, reflecting a transition in the Global South toward utilizing agricultural residues.

These innovative approaches are enabling the biofuel industry to move from high-cost R&D to commercially viable, scalable production while also eliminating supply chain volatility.

Supporting Infrastructure

Do you know it is more economical to trap the carbon dioxide produced by second-generation biofuel production processes than first-generation and conventional fuel production processes? Several biofuel production pathways, such as ethanol fermentation, lead to carbon dioxide emissions. Since the CO2 produced in the process is pure, the cost of purification can be skipped significantly. Thus, reducing the cost of CO2 capture as a whole. Several biofuel plants worldwide successfully capture carbon, pushing the total figure to 2.21 MtCO2 annually. However, to meet the 2030 Net Zero Scenario, they must scale this figure by 50 times. That can happen by filling the vast gap with better infrastructure deployment and development.

Policy Drivers Redefining the Feedstock Landscape

IEA laid out our four key priorities for rapid biofuel deployment, such as a comprehensive “sustainable fuels roadmap” with clear post-2030 targets for investment uncertainty. National biomass inventories help allocate feedstock effectively and prevent competition between sectors. Also, targeted grants and concessional finance are aimed at lowering SAF costs and speeding up commercialization. Transparent carbon accounting frameworks aligned with international best practices for CORSIA adherence.

Conclusion

The future of biofuels depends very much on alternative feedstocks for biofuels, as they enable the sustainable utilization of biomass, reduce competition with food, and offer lower carbon emissions. Better initiatives and efforts on multiple fronts can combat these predicaments. Governments and markets need to work hand-in-hand to understand the depth of these challenges and support new infrastructure and tech development. Simultaneous efforts can help cover the supply chain gaps and rising food crises. The world needs more programs like the Sustainable Aviation Grand Challenge Roadmap, which is currently active in the United States. Similarly, Germany dedicates huge investments and resources to improving yields from residues and wastes in Europe. Canada’s Clean Fuels Fund focuses on supply chain development for alternative fuels. Such initiatives are teamed with policies focused on emission reduction that promise incentives to biofuel producers to neutralize the emissions issue related to their production processes.

Stellarix’s energy consulting team supports companies in navigating the complex landscape of increasing ESG pressures and the demand for sustainable feedstock alternatives. We develop strategic roadmaps that combine in-depth research insights with comprehensive market analysis. Our actionable intelligence helps companies leverage the latest innovations in biofuel and renewable energy while ensuring compliance through R&D and sustainability consulting.

Let's Take the Conversation Forward

Reach out to Stellarix experts for tailored solutions to streamline your operations and achieve

measurable business excellence.