Can Food & Beverage Companies Build Their Brands without Contemplating DIY Food Kits in 2026?

Key Takeaways:

- The highest-margin entry point in the DIY food kit market is the underrepresented cuisines

- Skill-progressive kit formats are becoming the key to retaining customers

- Companies treating partner scouting as a post-development decision will lose the opportunity before the product is ready

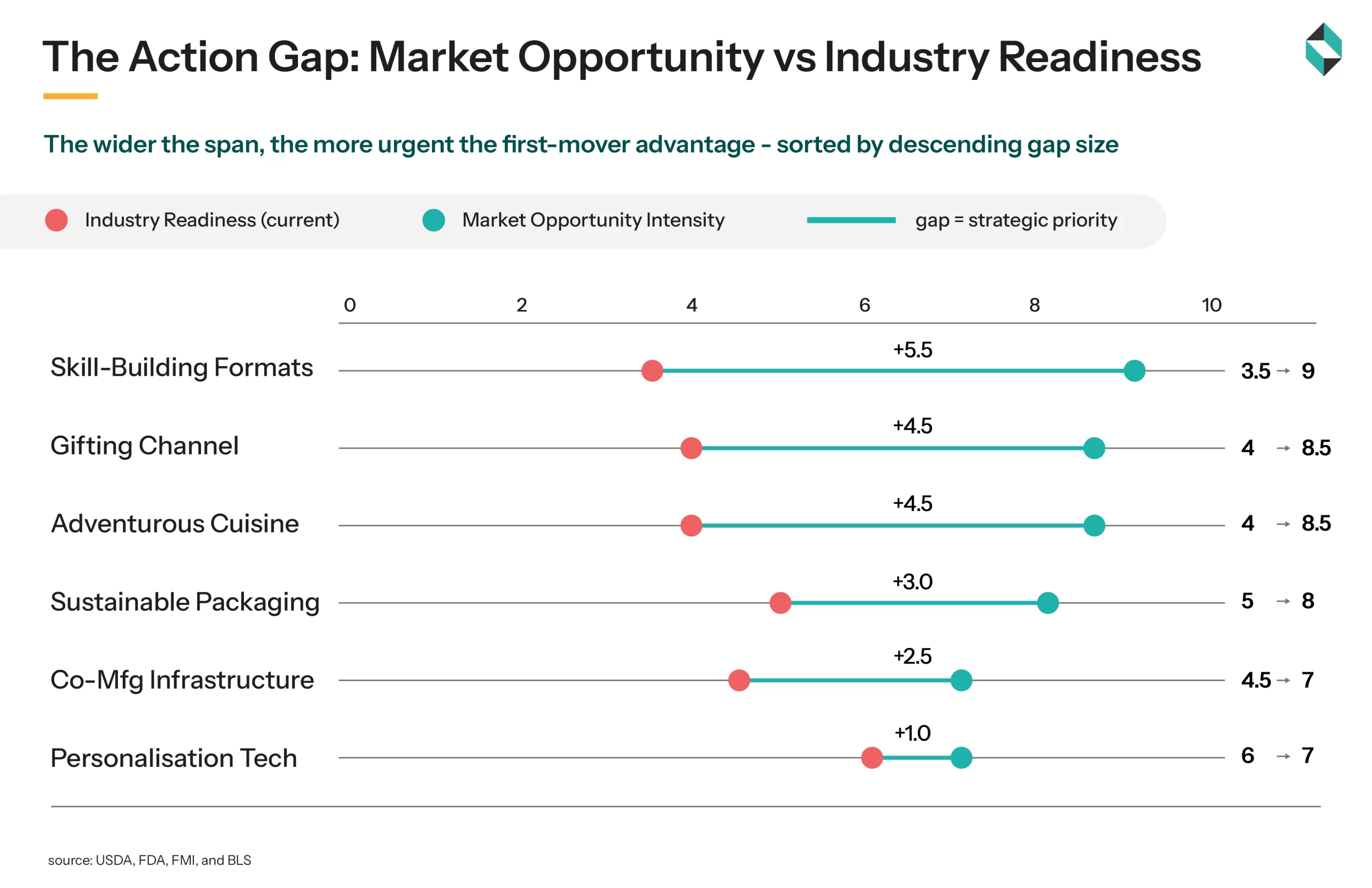

Almost every realignment signal for the food & beverage industry preceded changes in consumer behavior. The inclination towards organic entities was first registered in niche grocery aisles before it forced every retailer to change their procurement standards. The same goes for plant-based proteins; they entered as an ethical fringe and then turned into a multi-billion-dollar product genre. Along the same lines, DIY food kits are now maturing into a consumer habit. For market participants looking to chart new growth trajectories, this is a white-space window that opens doors to new opportunities. However, they may not remain open forever.

What makes 2026 so important is that since the first wave of make-your-own meal kits during the pandemic, customers’ expectations have compounded. Shoppers are now moving ahead of the basic protein, grain, and sauce format. They are looking for kits that teach, surprise, and align with their dietary frameworks. Additionally, these healthy home-cooked alternatives do not add to the plastic ice packs in the bins. However, each of these requisites is a supply chain and engineering challenge that demands margin-accretive solutions.

The strategic dilemma for retailers, co-packers, food makers, and ingredient innovators is whether their R&D pipeline, distribution infrastructure, and packaging partners are well-positioned to capture a significant market share before this gap is closed.

What Cues Can F&B Manufacturers Draw from the AI-driven Personalization Wave in this Niche?

The growing adoption of AI-driven personalization in DIY meal kit models and platforms is a demand signal story. When new market entrants like Gousto, HelloFresh, etc track dietary restrictions, cuisine inclinations, and preferences across countless orders through recommendation engines, they are focusing on individual eating choices, something manufacturers haven’t been able to do at a consumer level.

What this development offers to ingredient suppliers and food companies is asymmetric data exposure. More and more kit operators are accumulating demand intelligence, which is unavailable to established FMCG brands that heavily rely on infrequent market research and retailer scan data. The ingredient-by-ingredient knowledge of a kit operator who has catered to over 200, 000 consumers for a period of time could not be matched to deduce which flavor profiles drive churn and which ones will drive retention. It is proprietary information, especially with regard to product development assets that cannot be replaced by syndicated data subscriptions.

However, for companies considering AI personalization in their supply chain operations, margin management is an architecture challenge. A dynamic recipe substitution demands a fulfillment and purchasing system that could tailor execution at an individual level. Organizations that haven’t modeled the unit economics of per-SKU substitution often find out after a pilot that while the personalization dividend is real, operational cost is an enabling factor and is usually underestimated in most cases. So, should AI-based personalization be avoided altogether?

No, but its implementation should be systematic. The usual course of action is to begin with high-frequency substitution categories like grains, sauces, and proteins. At this stage, inventory turnover balances the system integration costs. They should move to low-frequency customization till the core platform gets margin-stable.

How DIY Meal Kits are Empowering Multiple Vectors from Premium Differentiation to Corporate Wellness Infrastructure?

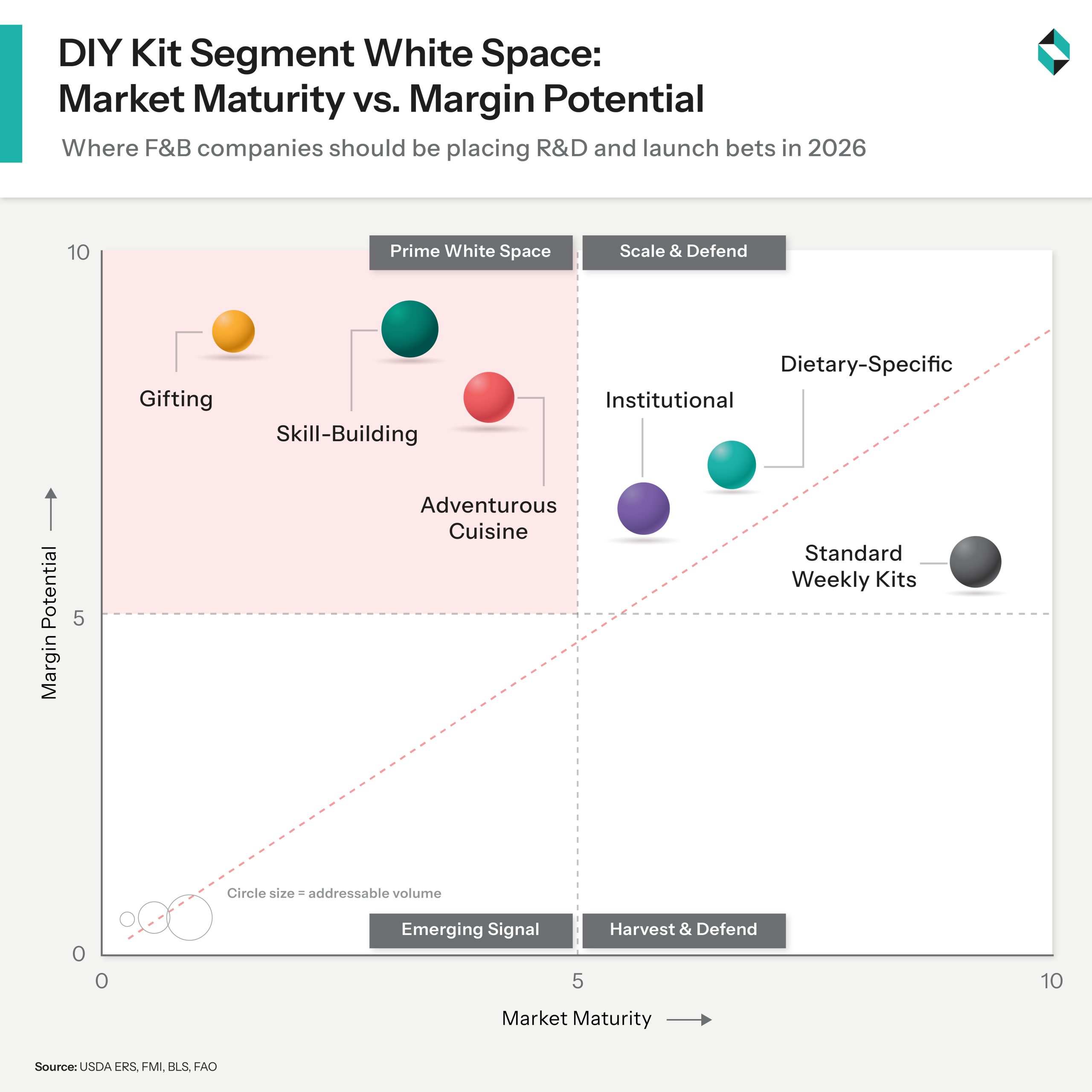

A recent consumer search highlighted a wide structural dissatisfaction with the regular meal kit value proposition. Most consumers who have been using these kits for over a year are actively seeking ready-to-cook meals that progressively teach more advanced techniques than the usual tricks offered by these kits. It is one of the most significant whitespace that is yet to be addressed by industry incumbents. There are a number of innovative formats that are leading this category, some of the best ones include:

- Artisan bread kits that teach proofing and scoring

- Fermentation kits, including everything from kimchi to miso

- Sushi kits engineered around knife techniques and rice seasoning

- Pasta kits spanning from tagliatelle to filled shapes

Key Takeaway: It isn’t ingredient cost but instructional architecture that is sustaining the premium price category in this segment.

Entry Vectors that Could Favor Manufacturers through Skill-building Kit Formats

- Ingredient Suppliers: Suppliers capable of offering pre-graded technique-appropriate ingredients could win supply lock-ins and premium contracts, unlike conventional commodity formats.

- Co-manufacturers: Skill-building kits need multi-component assembly like fresh components, dry pre-mixes, instructional inserts, and sauce packets in one thermally qualified unit. Co-packers with fresh-chilled and dry mixing integration ability are highly needed.

- Corporate Wellness: At-home cooking skills are identified as a fundamental driver of dietary quality. Skill-development kit programs in corporate wellness take care of both chronic disease cost drivers and retention engagement agendas emerging in self-ensured employer health data.

- CPG Brands: Ingredient incumbents have a straight way into skill-kit-co-branding and turning existing retail equities into DTC-compatible formats.

Key Takeaway: Food companies evaluating entry into the DIY food kits market, product design and development investments should be framed as a curriculum and content investments. It creates a defensible moat against private-label imitation. It’s true that retailers can replicate ingredient bundles, but they can’t replicate a 12-week fermentation curriculum rooted in proprietary recipe IP and supplier-exclusive component specifications.

Whitespaces Still Waiting to be Mapped

The gap is biggest between consumer demand for adult-oriented ready-to-cook meal kits and commercially available products. Time-constrained households with above-median income and culinary curiosity are looking for formats extending beyond the 30-minute weeknight dinners category.

The formats that are currently gaining consumer attention and appreciation include international cuisine kits and occasion-based adventure kits. The only thing common between these formats is the category logic that is more inclined towards experiential retail, but not grocery. The pricing architecture already reflects it.

In European markets, consumers are mostly attracted to Eastern Mediterranean, Peruvian ceviche, Levantine, and West African cuisines that are yet to be covered. Lastly, the economic advantage of most adventurous-cuisine kit formats is driven by the scarcity of ingredients and knowledge accessibility, and not raw material costs. For instance, a West African groundnut stew kit enjoys a 60-80% price premium, not because groundnuts and palm oil are costly, but because it is not easy to replicate the recipe from a supermarket.

“The meal kit operators with the nest unit economics aren’t the ones with the most recipes. The winners are the ones with the most disciplined component standardization underneath the appearance of personalization.” – Stellarix Observation

The Gifting Channel – an Untapped Revenue Opportunity

In the home-cooked alternatives gifts segment, DIY kits represent the most underdeveloped commercial channels. It is currently working at a price point that cannot be touched by standard subscription kits. Curated experience kits, like cocktail-paired charcuterie boards and Japanese ramen from scratch, currently fall under the price range of $60-$145 in the US for single-occasion purposes. These have a gift margin of 55-70%, something that weekly subscription kits can never replicate at equivalent COGS.

The gifting option neutralizes two structural challenges that can’t be addressed by subscription formats. First, the acquisition cost dilemma, and second, the seasonality problem. For companies with some brand equity, gifting options open up a path to the lowest barrier entry point in this segment.

Bottomline

The opportunity in this niche is not evenly distributed. It is more inclined towards specific, early movers. The white space with the highest margin in this space is in skill-progressive formats and underrepresented categories that are yet to be explored by market leaders. For those looking to secure a faster margin than DTC subscriptions, gifting channels and retail-placed kits present low-barrier entrance points. Along with that, substantial focus also needs to be placed on sustainable or zero-waste meal kits, which could help with brand and regulatory advantage that will become a fundamental necessity in the next three to four years. However, the planning cycles of most F&B companies are yet to calibrate for agile movement through this space. As an innovation partner, Stellarix is helping leadership teams to transform urgency into a well-structured action plan. From mapping cuisine white spaces to identifying co-manufacturing partners, our strategic support is compressing the analysis cycles for evidence-backed decisions.

Let's Take the Conversation Forward

Reach out to Stellarix experts for tailored solutions to streamline your operations and achieve

measurable business excellence.