How is the Current Supply Chain Crisis Testing the Resilience of Various Industries?

The supply chains that overcome this crisis won’t be the ones with the lowest cost structures, but those with decision-ready leadership. – Stellarix Observation

For years, international trade infrastructure was considered inviolable. This assumption was the bottom line for other assumptions that straits would stay untouched, ports would operate, and just-in-time would remain good. The picture started to erode in 2020 and finally shattered with the recent situation in the Hormuz.

What began as a small flashpoint has now expanded into a supply chain crisis for several industries. The Strait of Hormuz is the load-bearing wall of the global economy. The cracks of this wall are now impacting leaders from each industry, as several ends of the value chain, from raw materials to maritime logistics and energy, depend on it. In practice, it means almost every aspect of it.

Understanding the Scale of Global Supply Chain Disruption

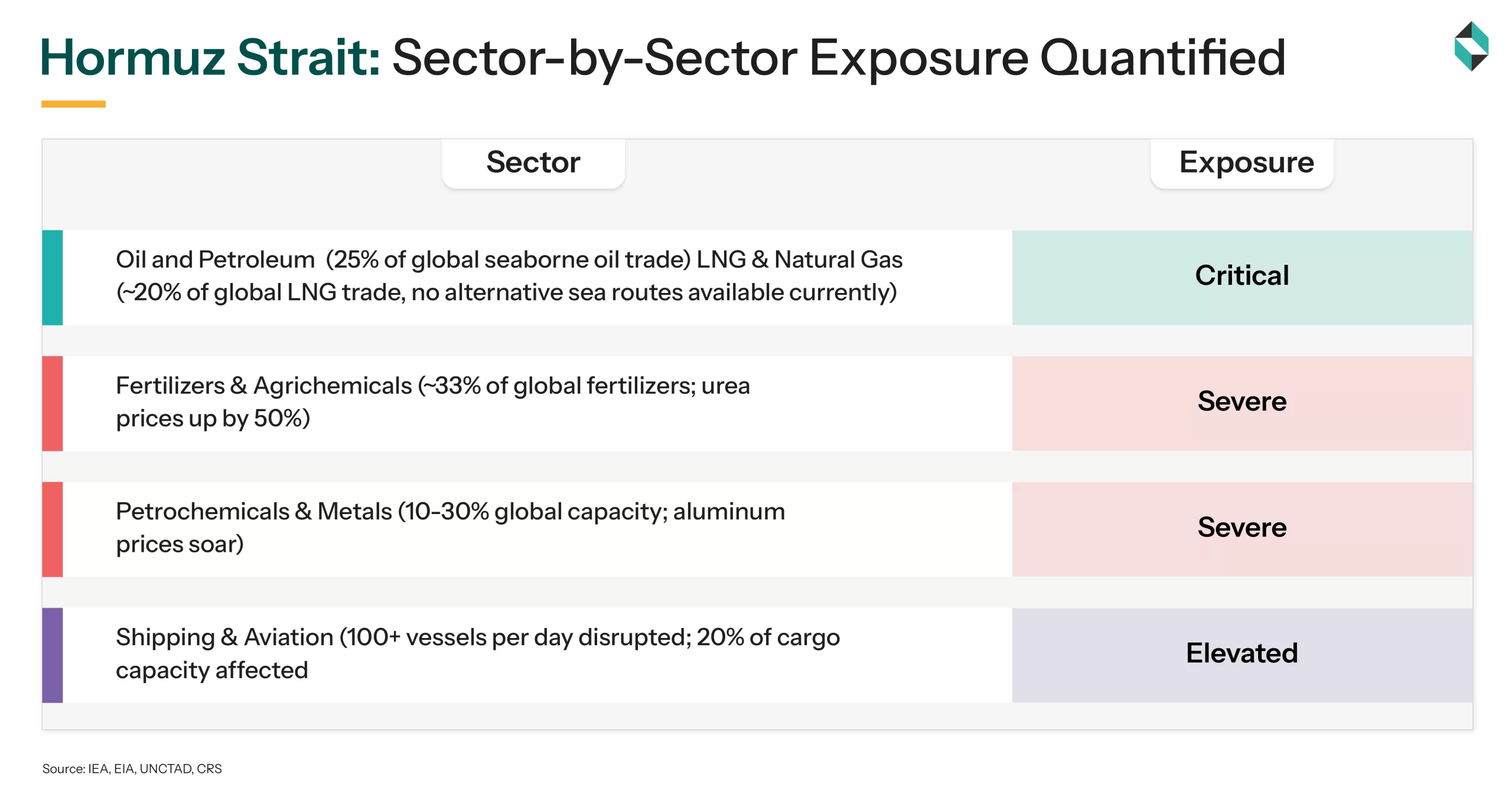

The scale of disruption in the global supply chain can be better understood through the quantification of its impact. As IEA reports, approx 20 million barrels of crude oil and other oil products transited the Strait every single day in 2025. This 25% of the world’s seaborne oil trade came to a halt and narrowed down to a trickle as Gulf nations slashed their daily oil production by over 11 million barrels. Simultaneously, the largest LNG liquefaction plant in the world, Qatar’s Ras Laffan facility, went offline since March 2, 2026, resulting in a loss of more than 2 billion cubic meters of global supply per week.

The ripples of energy shock are going wider and wider. Brent crude crossed $100 per barrel last month and is already reaching a peak of $126 per barrel. It also escalated natural gas prices in Asia and Europe by 54% and 63%, respectively, within a week. What makes this crisis structurally more intense and different from other disruptions is the lack of any reliable short-term buffer.

The IEA managed an emergency release of 400 million barrels, but volumetrically, it only covered a few weeks of net supply loss at the scale of a closed Strait. Here is a sector-by-sector assessment of its impact:

Industries Caught in this Crossfire

The sectors exposed to the acute pressure of this conflict aren’t just energy companies. Any industry relying on hydrocarbon-derived products, essentially most manufacturing sectors, is experiencing the secondary and tertiary effects of it.

Fertilizers

The fertilizer segment is bearing its secondary effects. The significant volumes of LNG transiting from the Strait power the fertilizer plants, along with urea, a core nitrogen fertilizer. With urea prices going up by 50%, agriculture is expected to feel its reverberations till 2027. If the conflict continues or goes on longer than now, these reverberation timelines will further extend. The most affected will be food production across the Northern Hemisphere, especially during the spring planting season.

Petrochemicals

A parallel line of impact is passing through the petrochemicals sector. 10-30% of the global capacity of the most critical chemicals comes from the Gulf region. This includes methanol, helium, and polyethylene. The disruptions in LPG and naphtha feedstocks are narrowing margins and compelling Asian producers to reduce operating rates. Meanwhile, the aluminum market is facing tightening premiums because Gulf producers are cut off from feedstock supply.

Aviation

Aviation and aerospace face a dual burden. As 20% of worldwide air cargo capacity is adversely impacted by the closure of Middle East airspaces. Jet fuel costs, which represent 25% of operating costs, have also gone up due to oil price spikes.

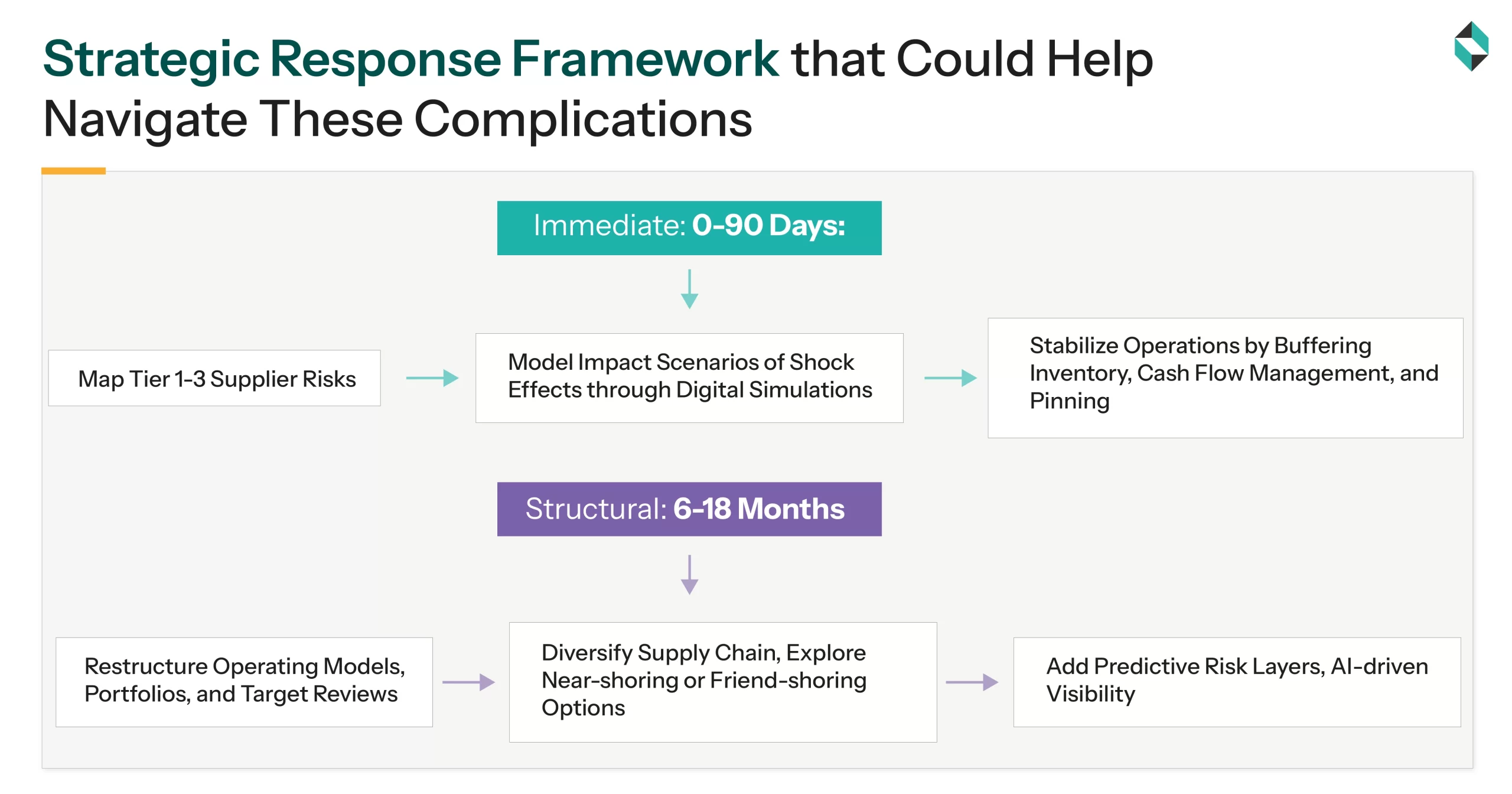

So, What’s the Way Out?

This crisis has accelerated the ideas that leadership teams were overlooking since 2022. The end of COVID-19 offered a short relief as supply chain pressures eased slightly, just-in-time orthodoxy returned, and resilience investments faced CFO scrutiny.

The current strategic imperative is now institutionalizing “just-in-case” strategies, suggesting a structural shift away from linear efficiency towards multi-vector sourcing and built-in redundancy. More and more leadership teams are now acknowledging that the cost of building resilience is definitely less than the cost of disruption. Approx. 71% of U.S. CEOs plan to modify their supply chains by 2030, reflecting restructuring as an enterprise risk strategy.

Bottomline

The present conflict is accomplishing what the last few disruptions did partially. Finally, industry leaders are recognizing that deliberate architectural investments to maintain supply chain efficiency and security together. The industries most exposed to these shocks are also the most interconnected ecosystems. From energy to chemicals, aviation, and agriculture, the ripples of this shock will continue expanding beyond the obvious flashpoints.

The strategic window for structural redesign is narrowing fast. Companies waiting for things to get back to normal may miss their chance for a competitive edge. Supply chain challenges of this level do not resolve quickly. So, leadership teams need to assess closely how they are architecturally equipped to respond.

As an innovation and strategy partner, Stellarix is working with chemical, energy, industrial, and manufacturing leaders to translate supply chain volatility into strategic clarity. Our consulting solutions are extending support from supply chain risk & scenario planning to strategic foresight, business & market strategies, operational resilience advisory, and strategic partner scouting.

Let's Take the Conversation Forward

Reach out to Stellarix experts for tailored solutions to streamline your operations and achieve

measurable business excellence.